Weekly Market Commentary - March 22th, 2025 - Click Here for Past Commentaries

-

The Federal Reserve left the fed funds rate unchanged this week, as expected,

and maintained its forecast of two interest rate cuts this year.

Bonds and international stocks are providing support for diversified portfolios,

with U.S. stocks pulling back from their February peak but recovering from correction territory.

Key economic readings out this week showed that, while growth is slowing from its above-trend

pace, the labor market remains healthy, and manufacturing sectors are improving.

-

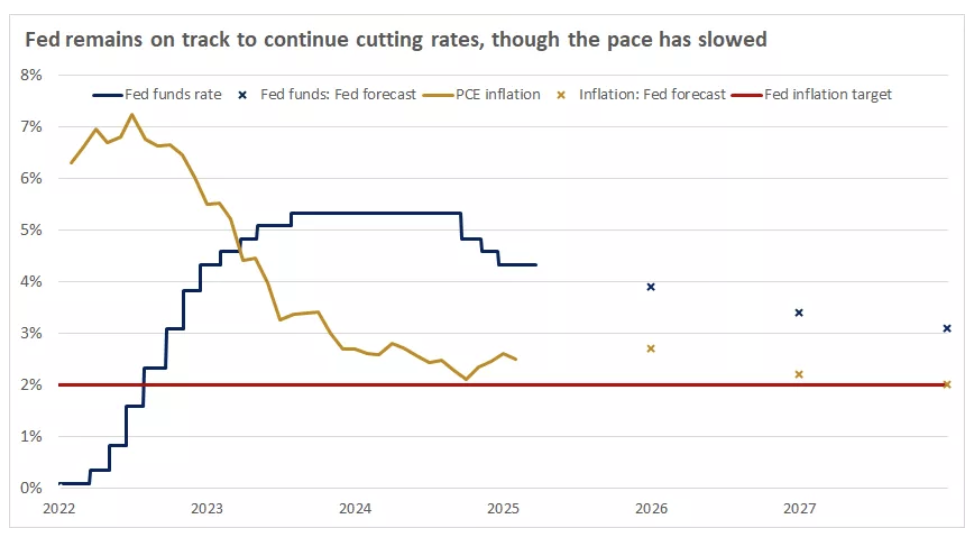

The Federal Open Market Committee (FOMC) concluded its March meeting this week, maintaining its

target range for the federal funds rate for the second consecutive meeting at 4.25%–4.5%, as expected.

The Fed is taking a more patient approach toward easing monetary policy amid slowing economic

growth and policy uncertainty.

The FOMC also updated its economic projections, with the fed funds rate’s “dot plot” still showing

two cuts each for 2025 and 2026. The outlook for economic growth for this year was lowered to 1.7%,

down from 2.1% in December. The FOMC raised its inflation expectations, with the Fed’s preferred

measure of inflation, Personal Consumption Expenditure (PCE), at 2.7% for 2025, up from 2.5% previously.

These projections show that the Fed expects tariffs to slow economic growth and trigger a one-time

adjustment in prices that leads to a short-term rise in inflation.

The Fed also announced it will slow its balance sheet reduction program, known as quantitative tightening (QT). Starting in April, holdings of U.S. Treasury securities will be reduced by $5 billion per month, down from $25 billion currently. Holdings of U.S. government agency debt and mortgage-backed securities will continue to decline by up to $35 billion monthly. Slowing quantitative tightening can help ease monetary policy, as the Fed will be able to participate in U.S. Treasury bond auctions more actively to replace maturing bonds. This additional demand should support bond prices, potentially helping to contain bond yields to the upside.

With the fed funds rate near 4.35% and PCE inflation at 2.5%, monetary policy becomes tighter as inflation moderates because a neutral rate is generally around 1% above the rate of inflation. We expect the Fed to remain on hold for a while longer as it awaits additional clarity on the implementation and potential impact of tariffs. The administration has indicated it intends to announce more details on tariffs in early April, which should help reduce uncertainty. Overall, we continue to believe the Fed remains on its easing path, though the pace has slowed, with the fed funds rate likely settling in the 3.5%–4.0% range this year. Lower interest rates should reduce borrowing costs for individuals and businesses, which is supportive of the economy and corporate earnings.

-

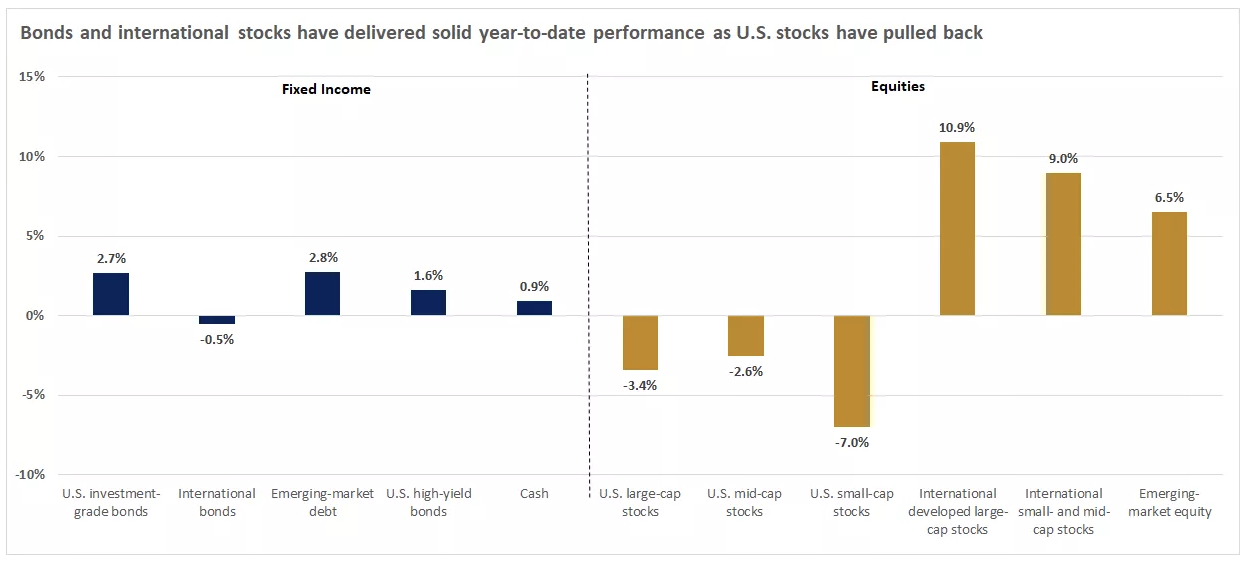

U.S. stocks were up slightly this week, recovering from correction territory, but remain down year to

date. Market leadership has rotated toward bonds and international stocks, providing support for

diversified portfolios.

International stocks have generated the strongest returns among the major asset classes so far this year,

led by developed-market large-cap stocks. Europe is benefiting from a multiyear plan to raise defense and

infrastructure spending that could help spur growth, which has been stagnant in recent years. The

potential for a Russia–Ukraine ceasefire has also improved sentiment.

Chinese stocks have risen on expectations for additional fiscal and monetary stimulus as the government seeks to boost consumption and head off deflation concerns. The pullback in the U.S. dollar from its January peak has also added to investment returns in major international currencies. U.S. bond yields have declined in recent months due to expectations for more Fed interest rate cuts and slower economic growth. Lower yields mean higher bond prices, which are driving solid returns. U.S. investment-grade bonds — the foundation of the fixed-income portion of portfolios — have delivered among the strongest returns within fixed income. Emerging-market debt has been the top fixed-income performer, extending last year’s strong returns and demonstrating the value of allocations beyond U.S. bonds.

-

The Conference Board’s Leading Economic Index (LEI) — which provides an early indication of significant

turning points in the business cycle as well as where the economy is heading in the near term — continued

its downward trend, falling 0.3% to 101.1 in February. Weaker consumer expectations for business conditions

and lower manufacturing new orders were the largest drivers of the decline, while higher weekly hours

worked for manufacturing were the main positive contributor.

Importantly, LEI’s six-month change, while still negative, remained on its upward trend and does not

signal a recession is imminent.2 These readings indicate that, while the economy faces headwinds, it is

slowing from an above-trend pace, and a recession is still not likely this year, in our view.

Initial jobless claims rose to 223,000 this past week, slightly below estimates of 224,000. Jobless claims have averaged about 227,000 over the past four weeks, modestly above the weekly average of 223,000 for 2024.3 While federal government layoffs will likely drive jobless claims higher in the months ahead, the labor market remains healthy, in our view. With the unemployment rate still low at 4.1% and job openings exceeding unemployment, wage gains should remain above inflation, providing positive real wages to support consumer spending and the economy. U.S. industrial production rose by 0.7% in February, ahead of expectations for a 0.3% increase.3 This was its highest level on record as businesses likely pulled forward purchases of inputs to get ahead of tariffs. Manufacturing output, which represents the majority of industrial production, increased by 0.9%, beating forecasts for a 0.3% rise and benefiting from a surge in automotive output. While this pace of output growth is likely not sustainable, the direction is consistent with other data that reflect a recovery in manufacturing is underway. This should help provide broader support for the economy and labor market.

We expect lower interest rates and pro-growth policies, such as deregulation and tax cuts, to help drive an acceleration in the economy later this year. Diversification has been key this year as U.S. stocks have pulled back. Consider adding to bond and international stocks in portfolios that may have drifted below their intended allocations.

-

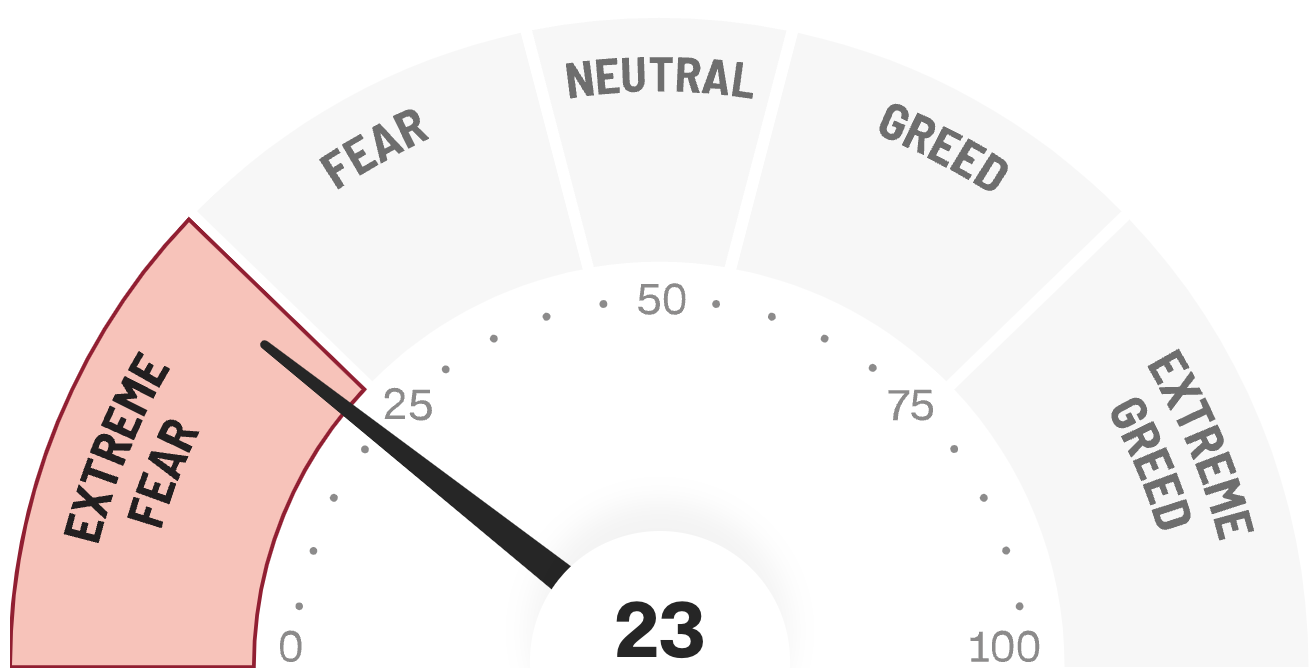

Final Words: Markets are at the all time high and fed is cutting

interest rate, caution warranted. Below is CNN Greed vs Fear Index, pointing at

'Extreme Fear'.

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

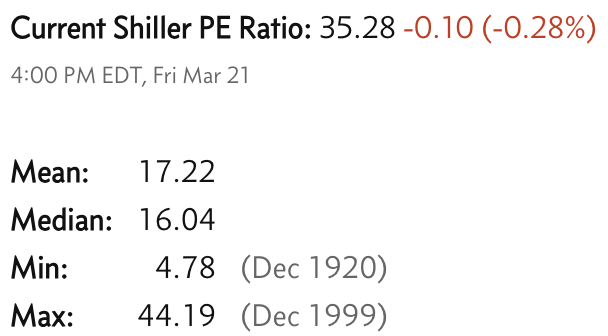

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.