Weekly Market Commentary - March 1st, 2025 - Click Here for Past Commentaries

-

Driven lower by mega-cap tech, the S&P 500 briefly erased its year-to-date gains but remains

15% higher from a year ago. A combination of growth concerns, trade uncertainty, and deteriorating

consumer confidence are contributing to the recent risk-off phase.

It is likely that the economy may go through a soft patch in the first half of the year and that

market volatility could stay elevated. However, we think there are enough supporting factors to

keep the economic expansion and bull market in stocks intact. These include positive economic

growth, a steady labor market, strong spending on AI, rising corporate profits, and a Fed that

remains in a rate-cutting cycle. The souring investor sentiment is helping take some froth out

of the market.

A run-of-the mill correction is possible but not inevitable, as stocks have already been moving

sideways over the past three months. A focus on balance and diversification can potentially better

help weather short-term dips, which over the long term are nearly impossible to avoid.

Diversification will be critical in 2025, and so far, it has shown its merits, as leadership has

broadened and rotated away from U.S. large-cap and tech, a trend that may continue.

-

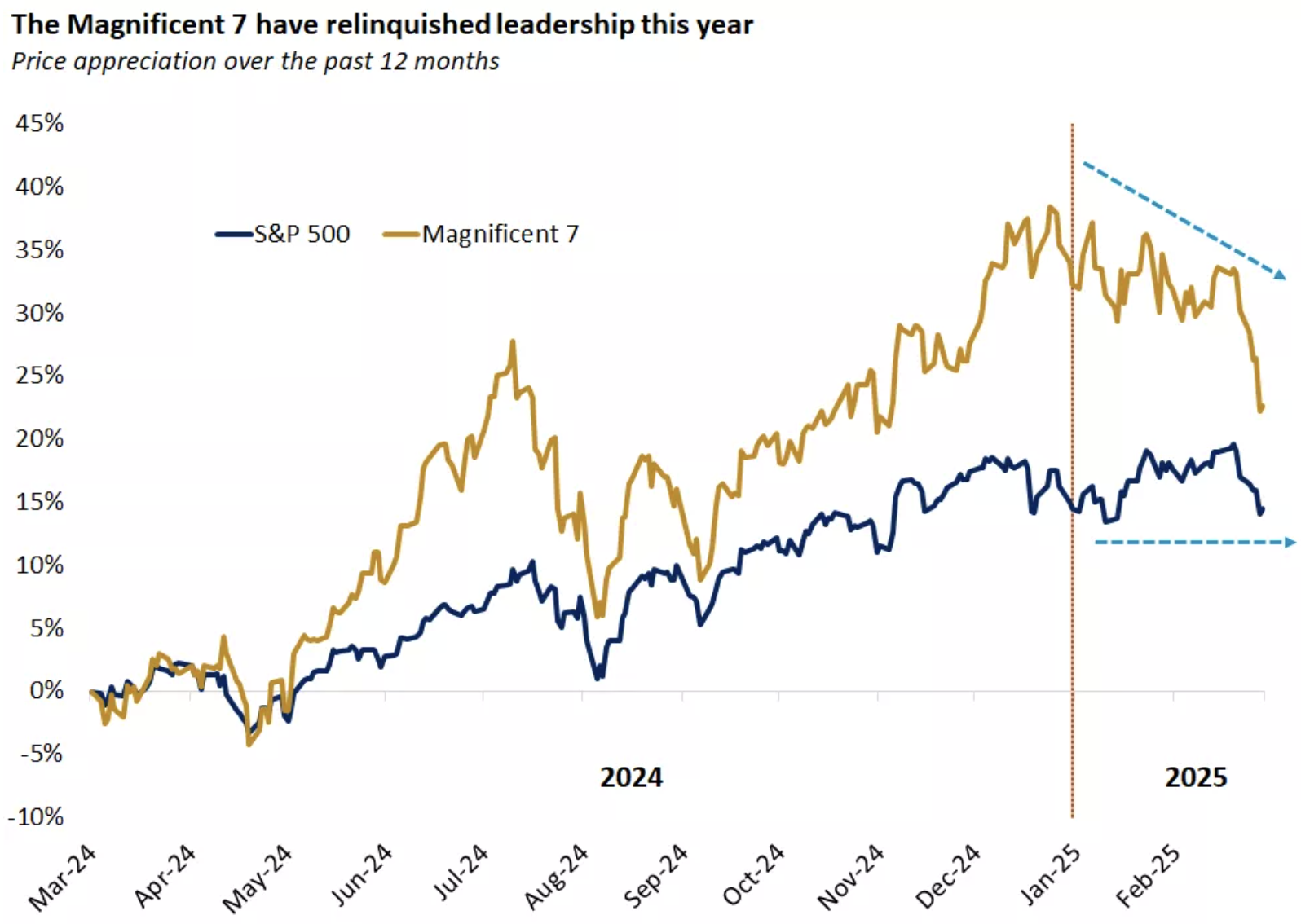

Last week, the S&P 500 briefly fell below last year's closing price, erasing the year-to-date gains,

and dropping 4.5% from its all-time high reached on February 19. Over the past two years, the

Magnificent 7 have driven more than 50% of the index's gains1. However, this year, the group has

shifted from a leader to a laggard, entering correction territory, while the broader index has

remained rangebound over the past three months.

To assess what's next for markets, we examine the key catalysts behind the recent pullback and

the factors that continue to support the economy and markets.

-

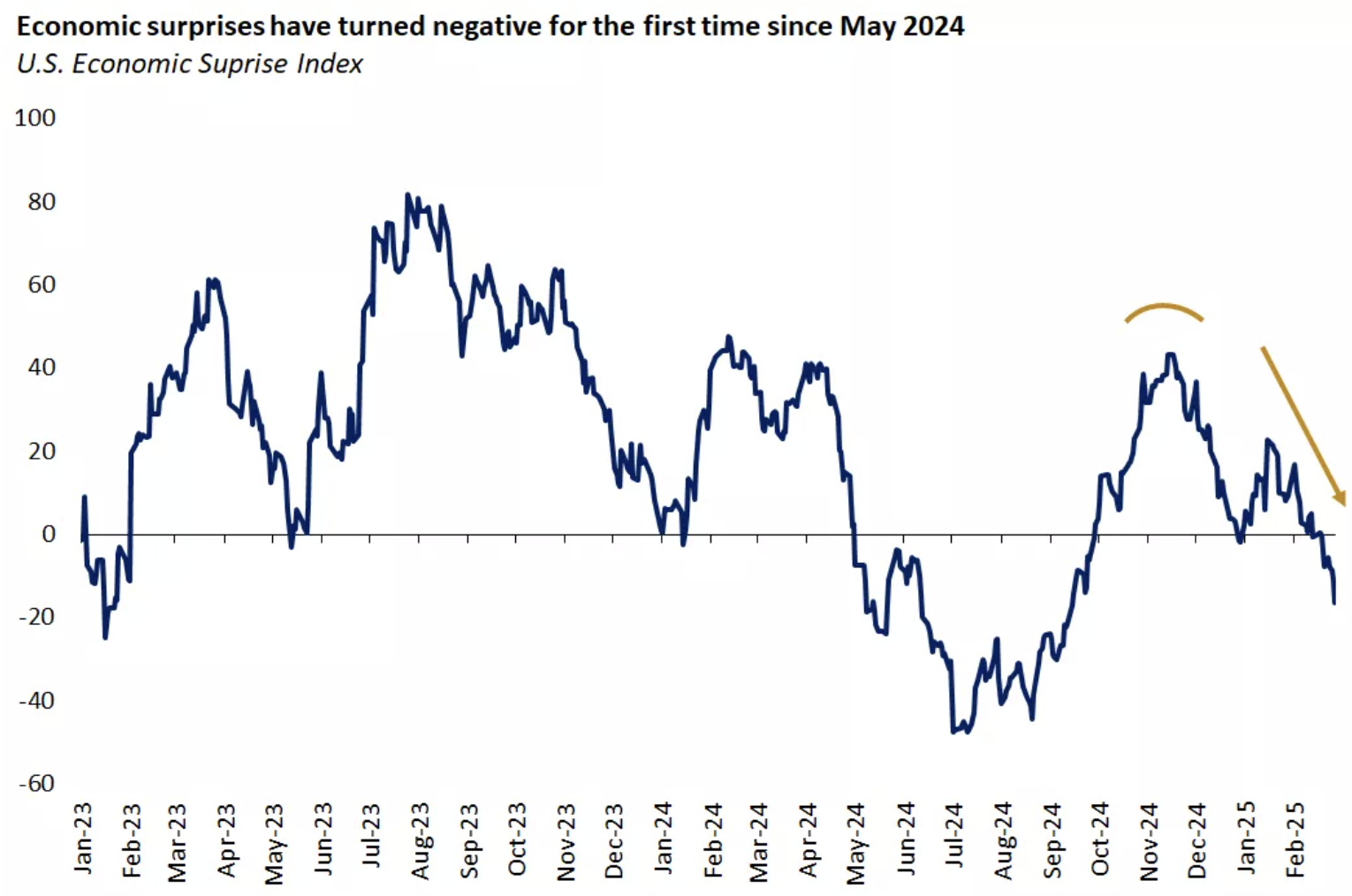

Last year, the U.S. economy delivered a strong performance, with GDP growing 2.8%. However, over

the past month a slew of economic indicators and surveys have surprised to the downside, suggesting

a loss of momentum in the first quarter of the year. January retail sales declined more than expected;

the S&P PMI - a key measure of business activity in the services sector - fell in contraction for

the first time in two years; initial jobless claims have risen; and the closely watched spread

between 10-year and 3-month Treasury yields has turned negative once again.

Without dismissing these signals (which we would characterize as yellow, not red, flags), it's important

to note that some of the weakness in activity may be due to unfavorable weather and snowstorms across

parts of the country, as some retailers have pointed out. Additionally, this is not the first time

markets have faced a growth scare during this cycle. Investors spent much of 2023 worrying about a

potential recession - a concern that never materialized – while also mistakenly expecting aggressive

Fed rate cuts following a brief uptick in unemployment in the summer of 2024.

-

Last week, President Trump said Canada and Mexico tariffs are on track to go into effect on March 4,

along with an additional 10% tax on Chinese imports. He also proposed new tariffs on the European

Union and reiterated that reciprocal tariffs are set for April 2. While so far it has been more tariff

noise than a tariff war, it seems likely that imposing levies on foreign goods is a core part of the

new administration's agenda.

The elevated trade-policy uncertainty is starting to weigh on sentiment, and, if it persists, may

prompt businesses to defer or cancel investments, and prompt consumers to pull back on spending.

While tariffs in isolation can lead to slower economic growth and drive a one-off increase in

prices, they should be considered as part of a policy mix that includes pro-growth measures that

would have an offsetting effect. Unlike the first Trump administration, this time the threat of

tariffs is coming before any potential tax cuts, contributing to the near-term investor worries.

-

With six of the Magnificent 7 companies already lagging the S&P 500 and the group falling out of favor,

all eyes were on NVIDIA last week, as the AI bellwether reported its quarterly results. Like past quarters,

the company experienced strong demand, with sales rising 78% from a year ago and exceeding consensus estimates

by 3%. While this rate of growth would be the envy of any company, the magnitude of positive surprise was

the smallest in eight quarters. The company also warned that profitability would be smaller than anticipated

as it rushes to roll out its new chip design. The upshot is that results were viewed as good but not great,

or a blowout, as they have been for most of last year. The 8.5% pullback in the stock following the

earnings release highlights how the bar of expectations is high and the ability to meet them is becoming harder.

-

Inflation worries, policy uncertainty and a choppy stock market have negatively impacted moods, as captured by

various consumer- and investor-sentiment surveys. The Conference Board’s Consumer Confidence Index for

February that was released last week declined for the third-straight month, recording its largest monthly

drop since August 2021. It remains to be seen whether the sour sentiment will negatively impact actual

activity, but we would note that an average of the two most popular consumer surveys was lower for most

of 2023, and consumer spending grew a solid 3% then. Consumers have been feeling lousy, but that hasn’t

stopped them from spending.

-

It is likely that the economy may go through a soft patch in the first half of the year and that market

volatility could stay elevated. However, we think there are enough supporting factors to keep the

economic expansion and bull market in stocks intact.

1. Economic growth is moderating from a strong starting point : Despite some of the recent underwhelming economic readings, consensus GDP estimates still call for a solid 2.3% growth for 20251. This figure may be revised lower if the administration follows an aggressive approach on tariffs, but even in that scenario, we don't expect domestic growth to be much weaker than the economy's 2% long-term potential. Consumer spending is likely slowing to a more sustainable pace, but it is not falling off a cliff. And on the business side, banks have begun to loosen lending standards on commercial loans, which, in combination with high CEO confidence, should support investment. We may see a soft patch early in the year, but that would be consistent with the pattern observed over the past 30 years, where economic activity in the first quarter has tended to be weaker on average relative to the other quarters.

2. Steady and healthy labor market : This week's jobs report will likely show that the unemployment rate remained at 4%, a historically low rate. A steady pace of job creation, with payrolls averaging 230,000 over the past three months, continues to support incomes and in turn consumer spending. And despite the lingering price pressures, wage growth has been exceeding the rate of inflation for 21 straight months.

3. Spending on artificial intelligence (AI) remains robust : While NVIDIA did not report blowout results, the company was positive on industry trends, describing demand for its chips as "extraordinary." The news about China's DeepSeek last month has triggered concerns about the pace of investments in the space. However, major players are not backing away from their spending plans to build the infrastructure needed. The declining cost curve of this technology will likely result in more companies embracing AI to drive productivity, a likely multiyear adoption process. The fact that the tech sector is losing some of its luster reflects the headwinds of elevated valuations and high expectations rather than an earnings issue, in our view.

4. Corporate profits are accelerating : In the near term stocks may be influenced by sentiment swings and headlines, but over the long term stocks tend to follow the path of corporate profits. With about 95% of the S&P 500 companies having reported results, the fourth-quarter earnings season is largely over. Profits grew 18% from a year ago, the highest quarterly earnings increase in three years. And full-year 2025 estimates are still pointing to double-digit growth, which provides a buffer for equities against any moderate decline in valuations that may take place this year.

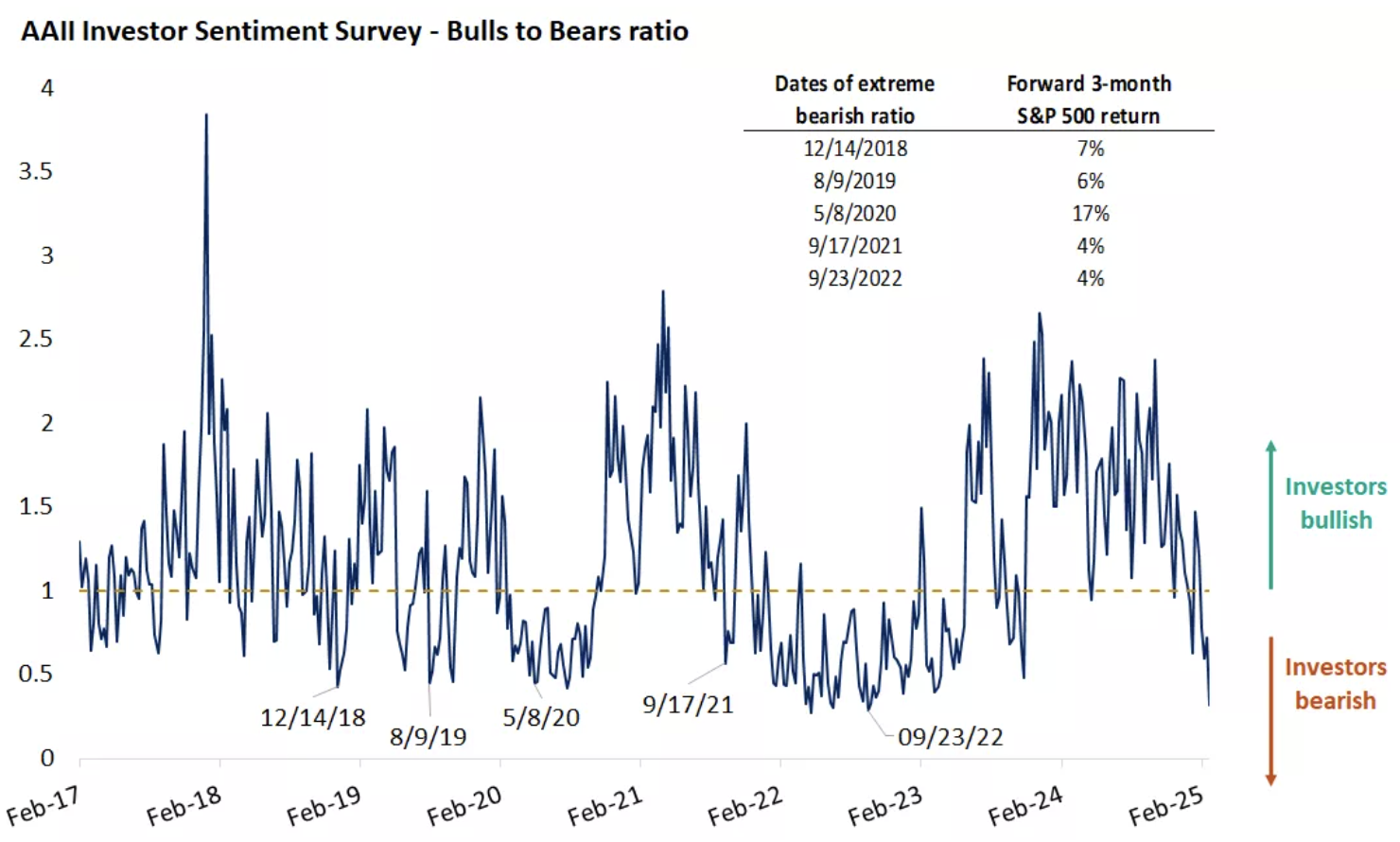

5. A reset in investor sentiment has helped take some froth out of the market : According to the American Association of Individual Investors (AAII), the percentage of investors that are now bearish (expecting the stock market to decline in the next six months) jumped to 61%, the highest since September of 2022 when the S&P 500 was down more than 20% from its peak. But sentiment is often a contrarian indicator. In the past whenever the bull-bear spread was as low as it is now, the pessimism has led to above-average forward three-month returns.

6. Inflation, though stubborn, remains in a downtrend : Despite the hotter-than-expected January CPI reading, the Fed's preferred measure of inflation, the core personal consumption expenditures price index (core PCE), came in at 2.6%, in line with estimates and lower than the prior month of 2.8%. While this is higher than the Fed would like it to be, the latest inflation data suggest that policymakers will be comfortable staying on the sidelines rather than bringing rate hikes back into the conversation. In fact, the recent drop in the 10-year Treasury yield from 4.8% to 4.25% reflects increasing chances that the Fed may cut rates more than one time this year.

-

The last time the S&P 500 experienced a correction (a 10% or more decline from highs) was more than a

year ago in October 2023. Given that over the past 100 years the market has averaged one of those

pullbacks a year, we may be overdue for one. However, a run-of-the mill correction is not inevitable,

as the sideways consolidation that we've seen in prices over the past three months may also be acting

as a corrective force. More importantly, even if the current pullback turns into a correction, we

don't think it will progress into something worse, as there are no signs of either an economic

downturn, a decline in corporate profits, or Fed rate hikes in the horizon.

Policy uncertainty and trade worries are a known unknown at this point and may keep volatility elevated in the months ahead. Investors can consider rebalancing strategies and dollar-cost averaging to take advantage of the wide price swings. As highlighted in our 2025 outlook, diversification will be critical in 2025, and, so far, it has shown its merits. Leadership has broadened and rotated away from U.S. large-cap, tech, and growth investments toward cyclical, value-style, and international stocks. Bond prices have also rallied, helping smooth out the bumps in equities.

A focus on balance and diversification can potentially better help weather short-term dips, which over the long term are nearly impossible to avoid. We maintain the view that equities have the potential to build on last year's strength, though with more moderate gains and higher volatility as market leadership continues to evolve.

-

Final Words: Markets are at the all time high and fed is cutting

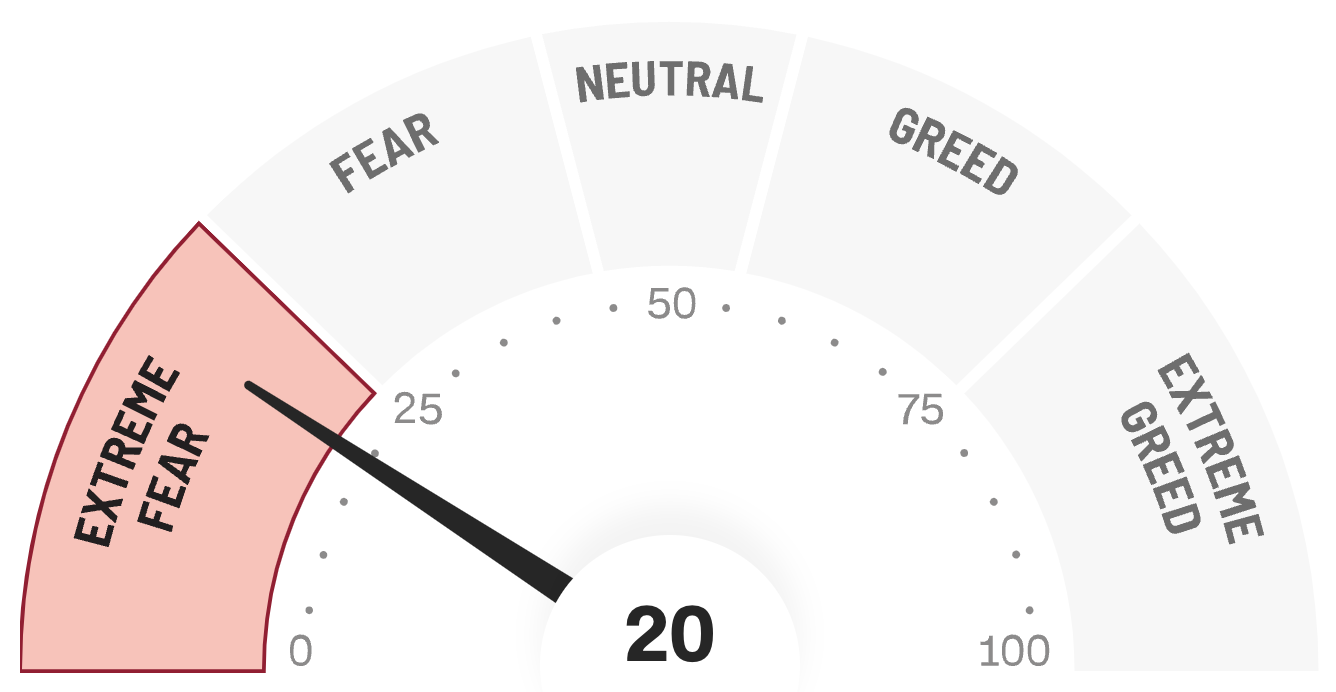

interest rate, caution warranted. Below is CNN Greed vs Fear Index, pointing at

'Fear'.

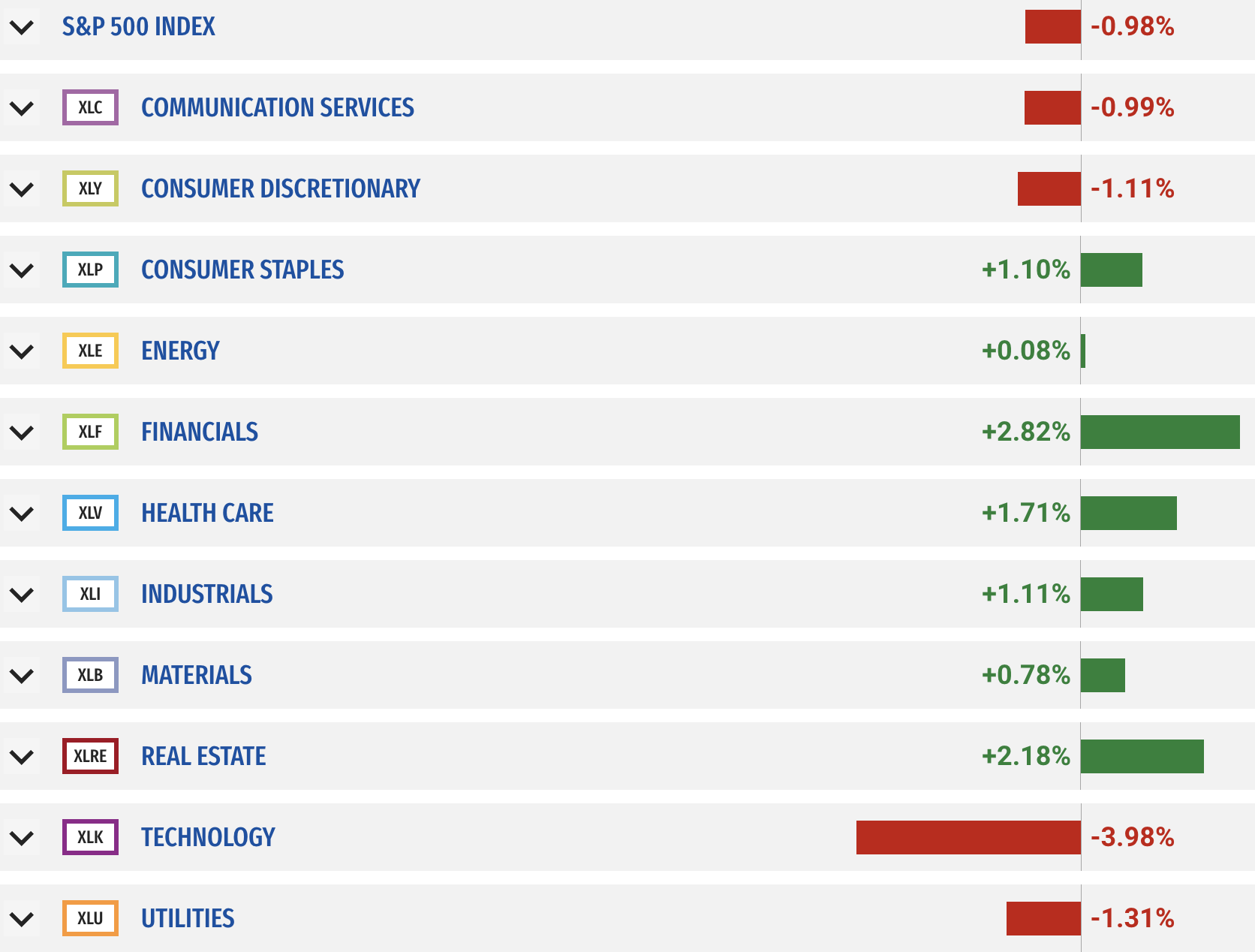

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

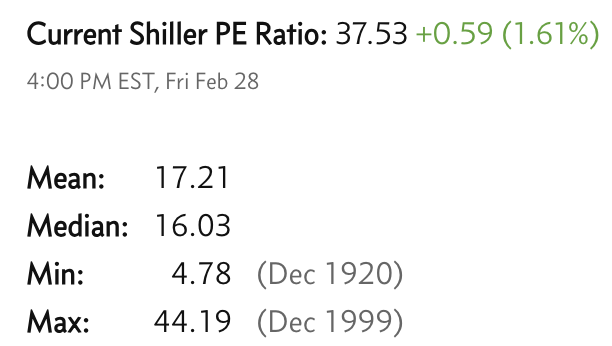

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.