Weekly Market Commentary - Jan 5th, 2025 - Click Here for Past Commentaries

-

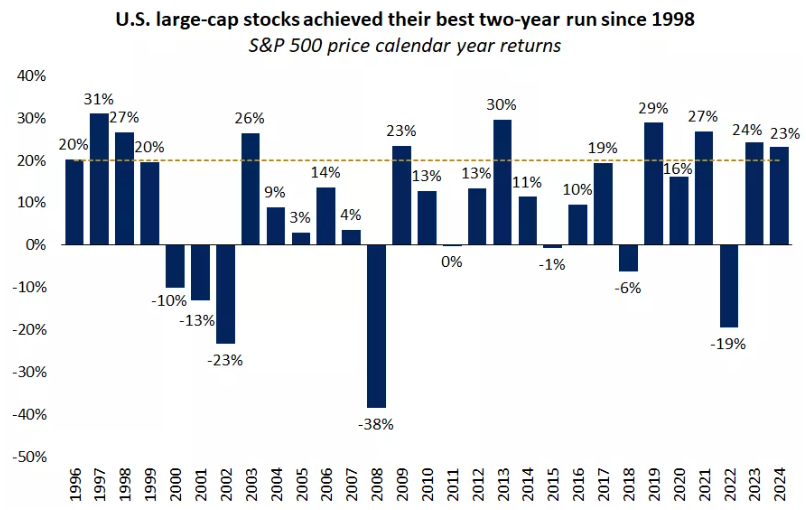

Despite an underwhelming end, 2024 proved to be a stellar year for investors.

The S&P 500 set 57 record highs and achieved its second consecutive year of 20%-plus

performance for the first time since 1998. Mega-cap tech led the way, but portfolios

enjoyed solid gains across sectors, styles and market caps. Now that 2024’s strong performance

is in the rearview mirror, it’s natural for investors to ask if the good times can continue.

We think 2025 will bring a mix of headwinds and tailwinds along with some policy uncertainty

around tariffs, taxes and interest rates. But ultimately, we believe stocks and bonds can build

on 2024’s gains, as the main drivers that propelled the stock market higher over the past 12

months appear poised to continue. We expect another year of healthy economic growth, rising

corporate profits and a continued normalization of Federal Reserve policy, all of which can

support the ongoing bull market.

-

Defying expectations for a sharper slowdown, the U.S. economy appears to have grown at a

2.7% pace in 2024 (including Q4 estimates). This is down only marginally from 2023’s 2.9% rate

and above the estimated long-term growth rate of around 2%. For 2025, we believe the U.S. economy

will continue to see positive but more moderate economic momentum.

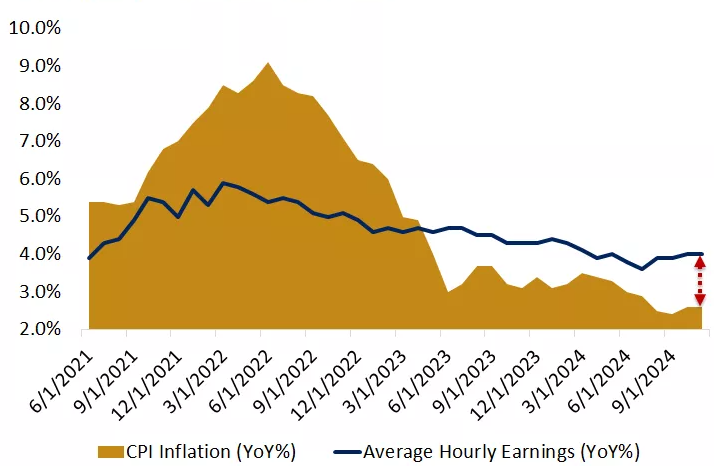

Consumer spending, which accounts for 70% of gross domestic product (GDP), remains supported by

a healthy labor market, wages that are rising faster than inflation, and appreciating real estate

and portfolio values.

Spending on services such as travel and hospitality is likely to slow after a period of

exceptional strength, but the U.S. manufacturing sector may stabilize and expand.

An “average” year — with GDP growing around its long-term potential — can validate expectations

of a soft landing and still provide a favorable backdrop for corporate profits to continue to grow.

-

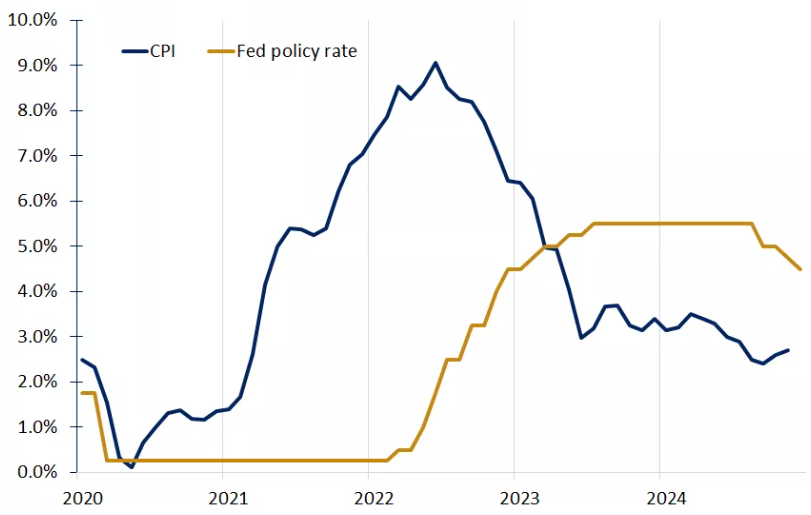

The Fed’s 0.25% rate cut and updated projections in December shifted interest rate expectations

higher, as policymakers now see fewer cuts in 2025. The economy continues to perform well, and there

is some uncertainty around how fast inflation will return to target, so the Fed is in no rush to cut rates.

However, the fed funds rate is now around 4.5%, well above inflation rates of about 2.5%. We

believe there is room to bring policy rates

down, likely settling in the 3.5% to 4% range in 2025. Two or possibly three rate cuts is a realistic

expectation, in our view, but there are uncertainties the Fed will have to navigate.

The new administration’s pro-growth policies and inflationary pressures could cause the Fed to cut

rates less than expected. On the other hand, any deterioration in growth could bring the Fed to cut

rates more than expected.

The good news is that we expect inflation to remain contained, without a return to rates above 4%.

The Fed will proceed cautiously as the last mile for inflation might be bumpy, but we still believe

inflation will continue its cooling trend.

- While treasury yields in the United States hit new 7-month highs, China's 10-year yield just hit a new RECORD low. In fact, China's 10-year government bond yield has now HALVED since January 2024.

- US equity funds saw a -$35.3 BILLION net outflow last week, the largest weekly outflow since December 2022. This is a sharp contrast to the ~$14 billion of weekly net INFLOWS seen since Fed interest rate cuts began.

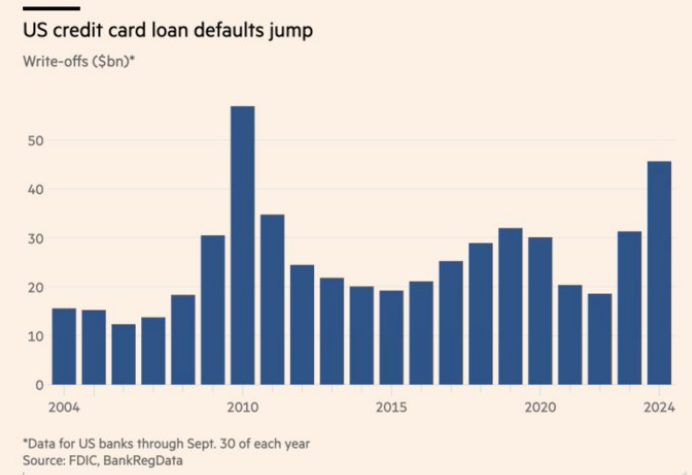

- Defaults on US credit card loans have hit the highest level since the wake of the 2008 financial crisis, in a sign that lower-income consumers’ financial health is waning after years of high inflation, per FT.

-

US credit card defaults jump to highest level since 2010. Credit card lenders wrote off $46bn

in seriously delinquent loan balances in first 9mths of 2024, up 50% from the same period in the

year prior and the highest level in 14yrs.

-

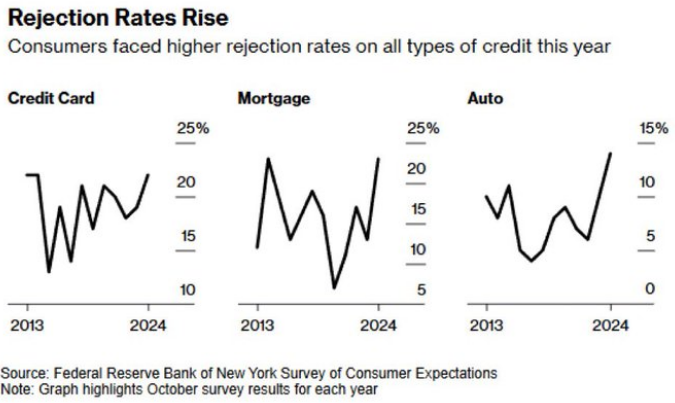

U.S. credit applications for mortgages and auto loans have currently been rejected at the highest

rate in ten years, per Bloomberg:

-

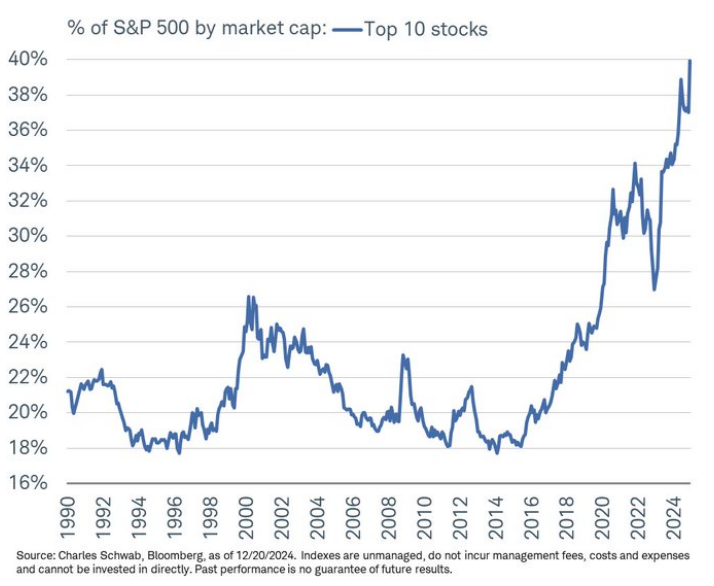

Top 10 stocks are now 40% of the US market.

It’s because they are tech infrastructure companies.

-

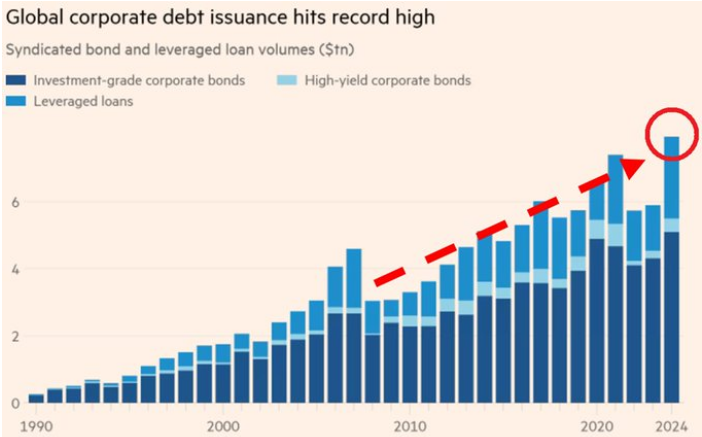

Global corporate debt issuance jumped ~34% year-over-year to a record $7.9 trillion in 2024.

Global corporate debt sales have DOUBLED over the last 12 years.

Issuances have now surpassed the previous record of $7.2 trillion in 2021.

This comes as historically low corporate bond spreads have fueled massive issuance activity.

Furthermore, the average US investment-grade bond spread has fallen to just 0.77 percentage

points in early December. This markets the tightest spread since the late 1990s, according to Ice BofA data.

-

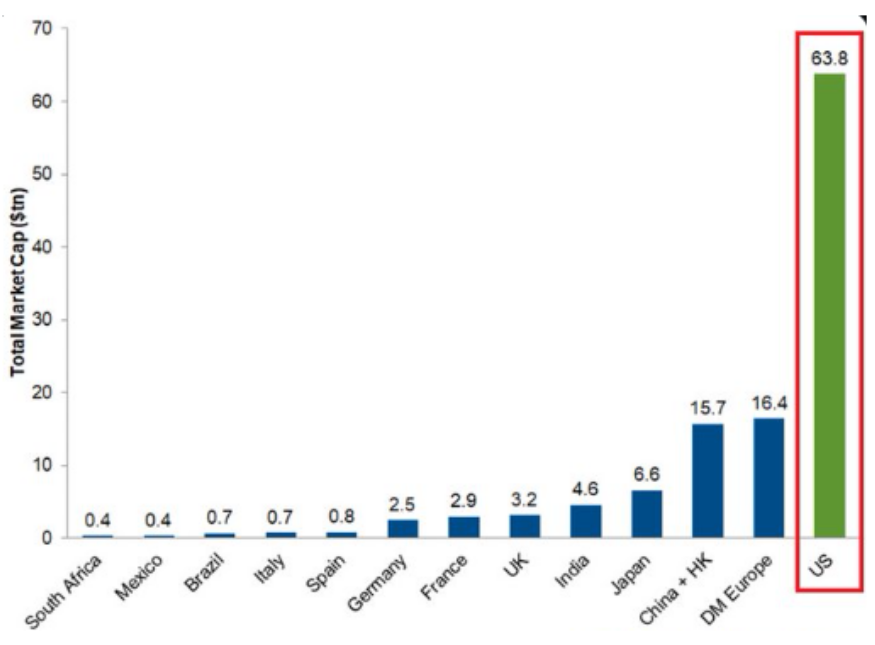

The US stock market is now worth a whopping $63.8 TRILLION, near an all-time high.

The US stock market's market cap has DOUBLED in just 4.5 years.

This year the market has added over $10 TRILLION in value.

To put this into perspective, China, Hong Kong, and Europe markets combined are worth ~50% less than the US.

The Magnificent 7 stocks' market cap alone is larger than the European market.

-

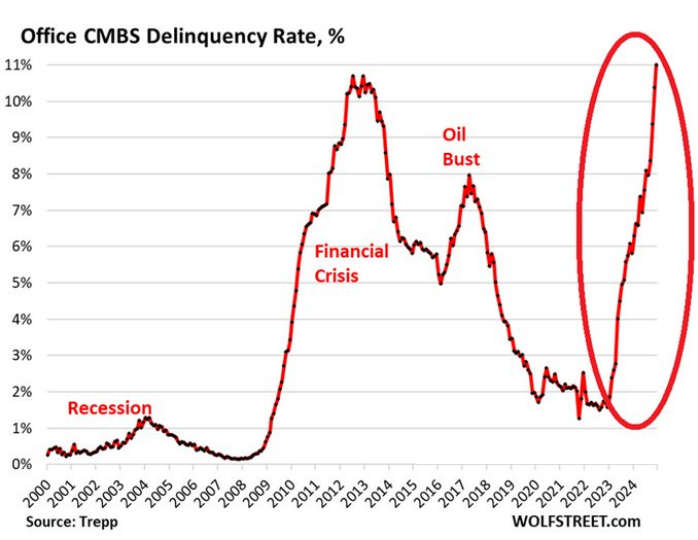

The delinquency rate on commercial mortgage-backed securities (CMBS) for offices jumped to a RECORD 11.0% in December.

Delinquency rates on these loans is now up 9.4 percentage points over the last 2 years

This puts delinquency rates above the 10.7% peak seen in December 2012.

Furthermore, delinquency rates on these loans are rising twice as fast as during the 2008 Financial Crisis.

Overall, there were more than $2 billion in office loans that became newly delinquent in December 2024.

The commercial real estate crisis is worsening.

-

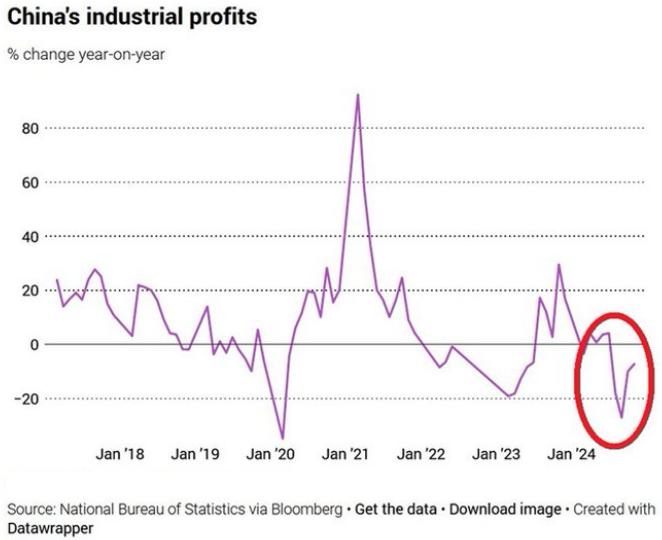

China’s industrial profits fell 7.3% year-over-year in November, marking the 4th consecutive monthly decline.

This comes after profits saw double-digit declines in the 3 previous months.

As a result, industrial profits are down 4.7% for the first 11 months of 2024, on track for the largest annual drop on record.

Low domestic demand was behind the recent weakness even as widespread stimulus has begun.

Will China enter a recession in 2025?

-

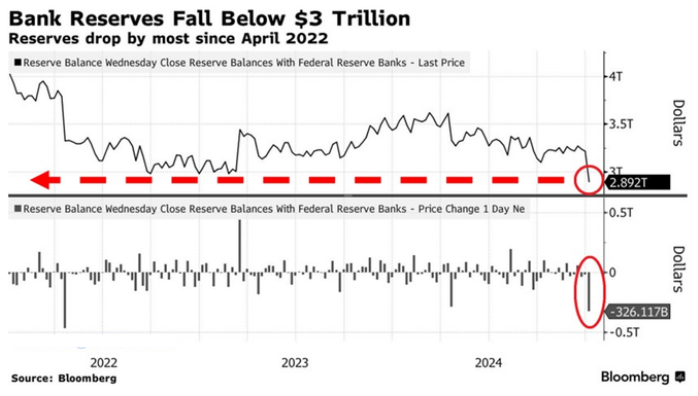

Bank reserves dropped by $326 billion in the week ending January 1st, to $2.9 trillion, the lowest since October 2020.

This marks the largest weekly decline since April 2022.

Since the September 2021 peak, reserves have declined by a whopping $1.3 trillion.

-

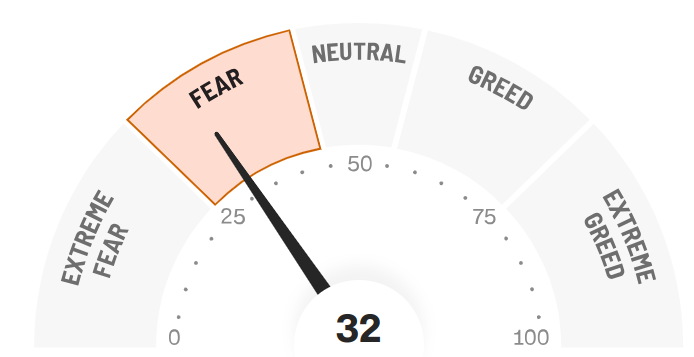

Final Words: Markets are at the all time high and fed is cutting

interest rate, caution warranted. Below is CNN Greed vs Fear Index, pointing at

'fear'. This maybe a good time to buy ETF such as VOO.

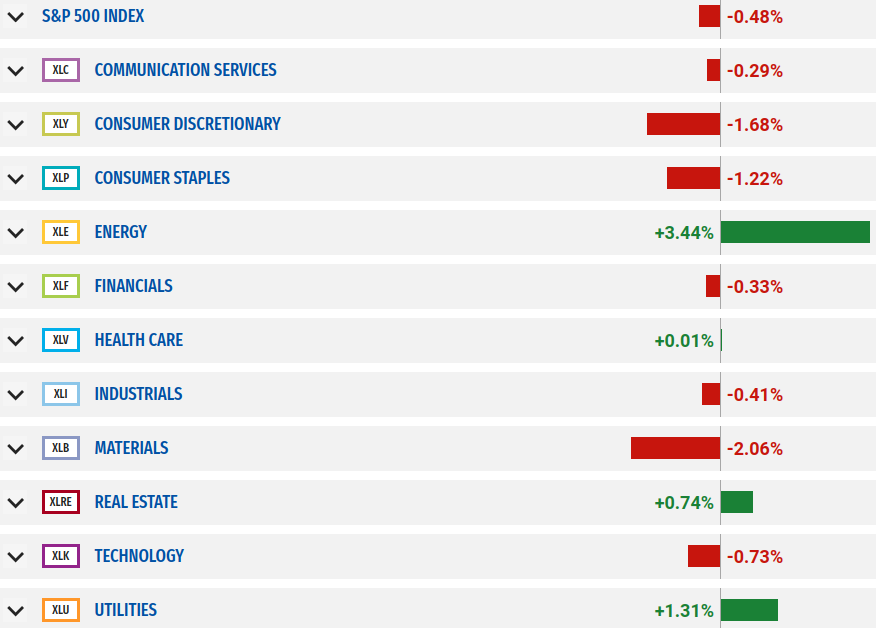

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

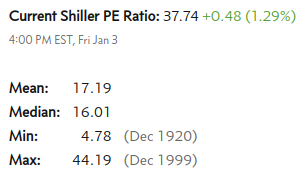

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.