Weekly Market Commentary - Jan 31, 2026 - Click Here for Past Commentaries

-

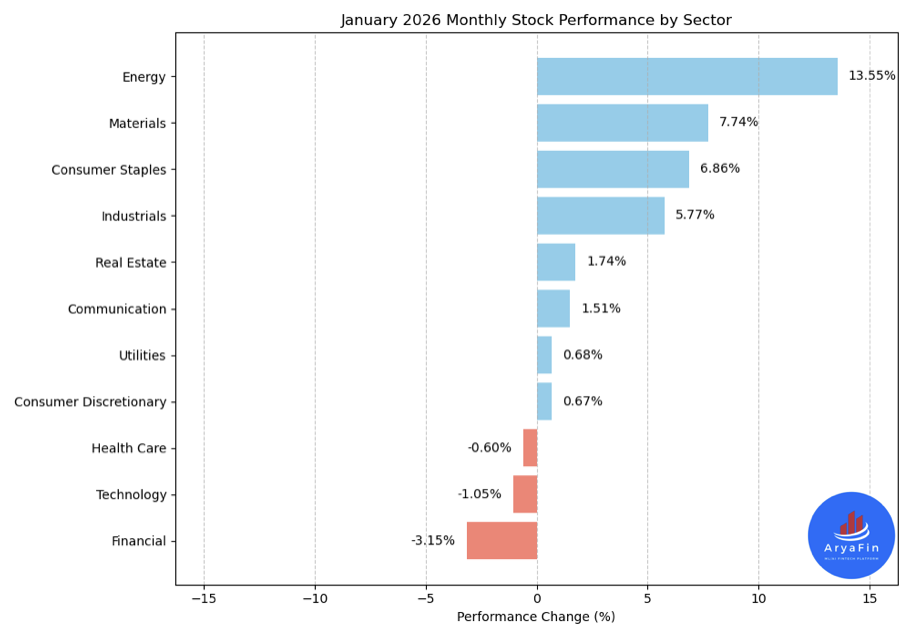

Energy (13.55%) and Materials (7.74%) were the top-performing sectors in January. Financials and Technology were the weakest. Technology companies continue to post strong results, though valuations remain elevated. The Fed held rates steady, as expected, following three consecutive cuts late in 2025. The pace of easing is likely to slow as policymakers seek further confirmation that inflation continues to cool.

Kevin Warsh—Federal Reserve Board member from 2006 to 2011—was nominated to succeed Jerome Powell as the next Fed Chair.

Warsh’s nomination likely signals a dovish shift on interest rates relative to Chair Powell, though his influence will be tempered by the Fed’s structure, including the 12-member voting FOMC.

Earnings season is in full swing, with key Magnificent 7 companies reporting results that beat estimates.

Congress reportedly reached a deal to extend funding for most of the government, though a partial shutdown still appears likely over the weekend.

-

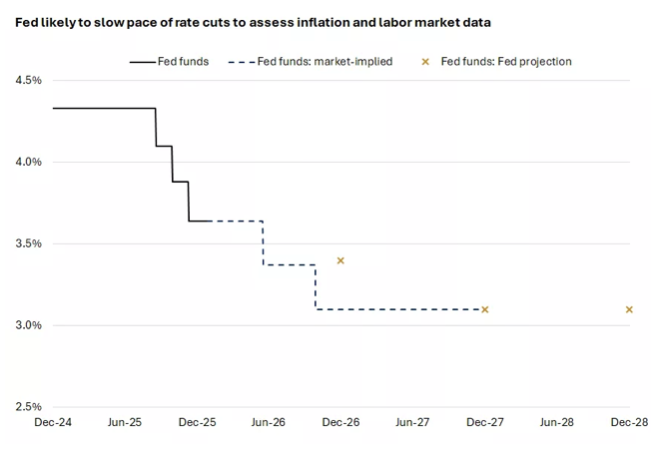

The Federal Open Market Committee (FOMC) concluded its January meeting by maintaining the federal funds target range at 3.5%–3.75%. The FOMC upgraded its assessment of the economy, noting that activity is expanding at a solid pace, supported by resilient consumer spending and rising business investment. The statement also reflected the committee’s view that, although job gains have slowed, the labor market has improved and shows signs of stabilization, even as inflation remains elevated. In our view, this language suggests the Fed is adopting a more patient stance after three consecutive rate cuts late last year.

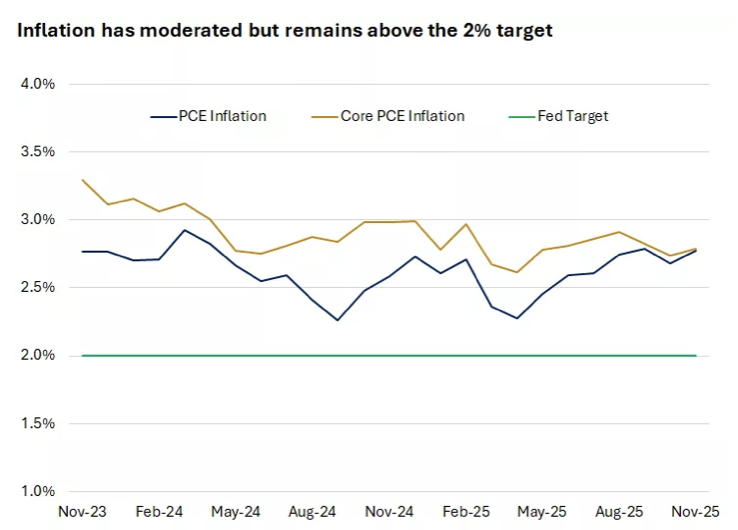

The Fed’s preferred inflation gauge — the Personal Consumption Expenditures (PCE) price index — has moderated, helped by cooling services inflation. Partially offsetting this progress, goods inflation has risen, partly due to tariffs. Overall, inflation remains above the 2% target, and the pace of disinflation has slowed.

We expect tariff-related price pressures to begin fading around midyear. Much of the impact reflects one-time price-level adjustments implemented in mid-2025, meaning the effects should gradually roll out of year-over-year inflation comparisons. We expect the Fed to resume rate cuts once policymakers have more data confirming that inflation is cooling toward target.

As outlined in our report, Kevin Warsh, nominated as the next Fed Chair, brings credibility and experience, including a key role during the 2008 financial crisis. While his monetary-policy views have been mixed, we expect Warsh to be more supportive of rate cuts than Chair Powell. He contends that the U.S. is entering a period of higher productivity—driven by new technologies (including AI) and potential deregulation—which could support faster growth with contained inflation.

Warsh has also been a vocal critic of the Fed’s balance sheet, calling it too large. He asserts that the Fed’s bond holdings expanded excessively through multiple rounds of quantitative easing. In his view, inflation risks associated with rate cuts (monetary easing) could be mitigated by shrinking the balance sheet (monetary tightening). Warsh believes this policy mix can support growth, based on his view that low interest rates benefit the economy more than maintaining a large Fed balance sheet. He also considers the Fed’s approach to inflation forecasting outdated, advocating for broader perspectives to be considered.

We expect Warsh to ultimately be confirmed by the Senate, but the process may take time. Republicans hold a narrow 13-11 majority on the Senate Committee on Banking, Housing and Urban Affairs (Senate Banking Committee), which reviews Federal Reserve Board nominees—including the chair—before sending them to the full Senate for final confirmation. Republican committee member Thom Tillis has indicated he will oppose confirmation of any Fed nominees until the DOJ investigation into Jerome Powell regarding Fed building renovations is resolved.

If Warsh’s confirmation extends beyond the end of Powell’s term as chair in May 2026, Vice Chair Philip Jefferson would temporarily serve as acting chair. Powell’s term on the Fed Board ends in January 2028, though how long he might remain is unclear. In response to the DOJ investigation, Powell stated that he intends to continue in his role, citing the need for public servants to stand firm in the face of threats.

The Fed chair is highly visible and exerts notable influence over monetary policy and communications. However, that influence is intentionally constrained by the Fed’s structure, which is designed to preserve independence, including:

- staggered 14-year terms for the seven Board members;

- independent board appointments of the 12 regional Federal Reserve Bank presidents to five-year terms;

- removal only “for cause,” which has never occurred—“cause” is not explicitly defined but has historically been interpreted as neglect of duty or malfeasance; and

- equal votes for all 12 voting members, who routinely express independent views.

Several Fed officials have recently emphasized the importance of central-bank independence. While some members may show deference to the chair, we expect continued diversity of views and data-dependent decisions.

If Fed independence were called into question, markets might react by pricing in uncertainty, potentially lifting intermediate- to long-term yields, steepening the yield curve, and pressuring bond prices.

Fourth-quarter earnings season hits its stride this week, with Magnificent 7 companies Apple, Meta Platforms, Microsoft, and Tesla reporting results that all beat estimates. Stock reactions were mixed, with Microsoft trading sharply lower due to concerns over robust capital-expenditure spending and slower cloud-computing growth.

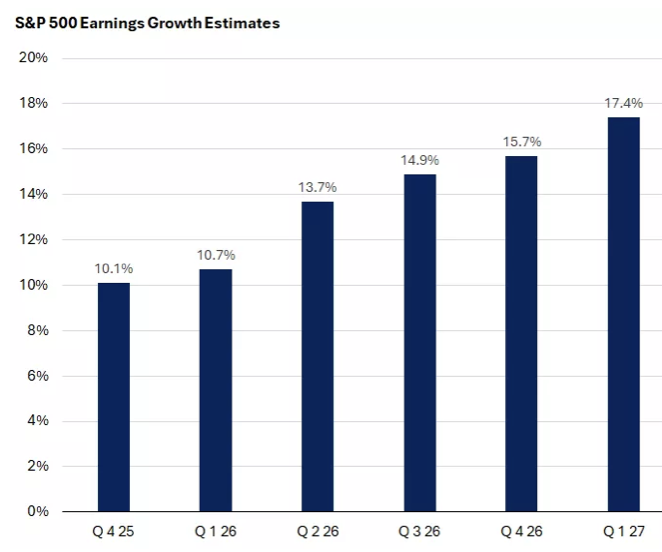

Earnings for S&P 500 companies are expected to rise about 10.1% year-over-year in the fourth quarter, led by the technology sector with over 25% growth. Earnings growth is expected to be broad-based, with eight of the 11 sectors forecast to report higher earnings. We expect strong earnings growth to support a broadening of market leadership. Robust profit growth is expected to accelerate into 2027, as shown below.

The short-term funding package that ended the 2025 government shutdown expired on January 30. Congress has reportedly reached a deal to extend funding for most of the government through September 2026. However, a partial government shutdown over the weekend appears likely, as the package requires approval by the House of Representatives, which is scheduled to return to session on February 2.

Democratic Party leaders have indicated that they will not support funding for the Department of Homeland Security (DHS) until the Trump administration agrees to reforms to Immigration and Customs Enforcement (ICE) and Customs and Border Protection (CBP) immigration-enforcement operations. DHS funding may be excluded from the package pending the outcome of negotiations.

From an economic standpoint, we would expect a short-term slowdown in growth around the shutdown period but a quick recovery in activity in the subsequent weeks and months. In other words, a shutdown would displace or delay spending and economic activity, not eliminate it, in our view.

The Fed chair announcement does not change our outlook for the Fed to cut rates once or twice this year, targeting 3.0%–3.5% for the fed funds rate. The pace of easing is expected to slow.

With the federal funds target range at 3.5%–3.75%, policy appears close to neutral, in our view. PCE inflation is running at 2.8% annualized, and a neutral policy rate is generally estimated at roughly 0.75%–1% above inflation for the U.S.

The Fed should be able to resume rate cuts, in our view, assuming price pressures continue to ease. We think a stabilizing labor market—characterized by modest hiring and limited layoffs—should help give policymakers time to confirm that inflation is moving toward the target.

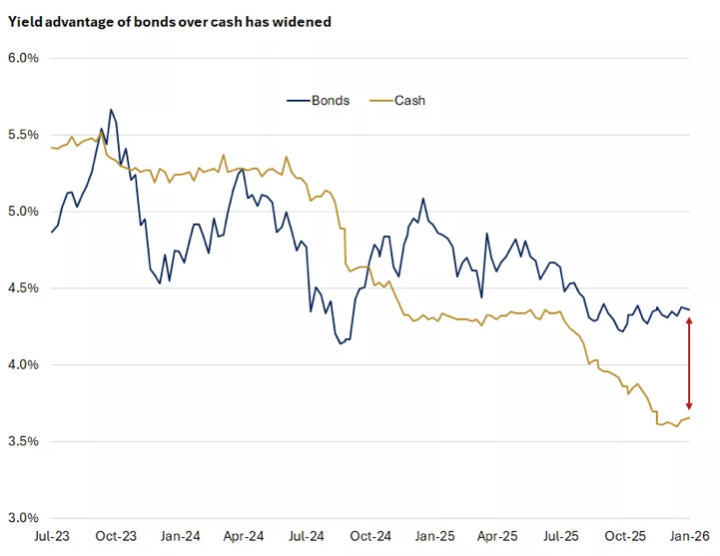

Cash yields have fallen in recent years alongside Fed rate cuts. Additional Fed Treasury bill purchases should help anchor the short end of the yield curve near the fed funds rate, likely pushing cash yields lower.

By contrast, we expect the 10-year U.S. Treasury yield to remain largely within the 4.0%–4.5% range this year—still near the upper end of its range over the past two decades. A positive yield curve should help keep intermediate-term bond yields above fed funds. Resilient growth, persistent budget deficits, and inflation risks typically drive yields higher, making a sustained drop unlikely, in our view.

Some investors may be overweight cash-like investments, including money market funds, which drew significant inflows amid elevated yields. Consider gradually reinvesting excess cash into either quality bonds that carry more attractive yields or equities aligned with your goals and risk tolerance.

A backdrop of easing rates, resilient growth, and rising earnings should help support equities relative to fixed income, in our view. We favor U.S. large- and mid-cap stocks, where we think leadership should continue to broaden. International developed small- and mid-cap equities and emerging-market equities may benefit from global economic resilience, lower valuations, and potential U.S. dollar softness.

Within fixed income, we think international bonds can add diversification through exposure to different economic and interest-rate cycles, while emerging-market debt can also enhance income potential.

In our view, Warsh's nomination likely represents a dovish shift for the Fed chair role, but the impact should be tempered. We continue to expect one or two Fed rate cuts this year, assuming price pressures continue to ease. This interest-rate backdrop, together with resilient growth, rising earnings, and potential U.S. dollar softness, supports the case for diversification and a broadening of equity-market leadership.

-

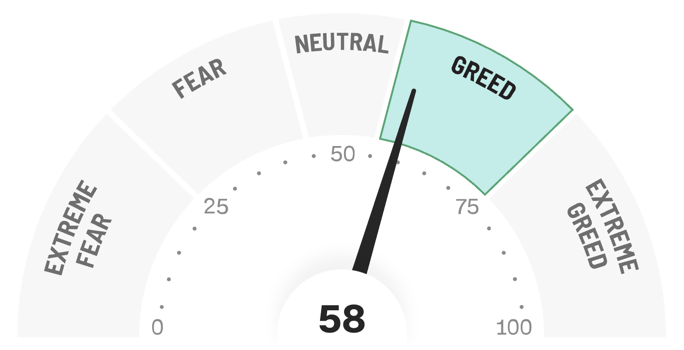

Final Words: Market indicates Greed. New Buys Copper (ICOP) & Pfizer (PFE)

Below is last week sector performance report.

Monthly Sector Performance for January 2026:

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

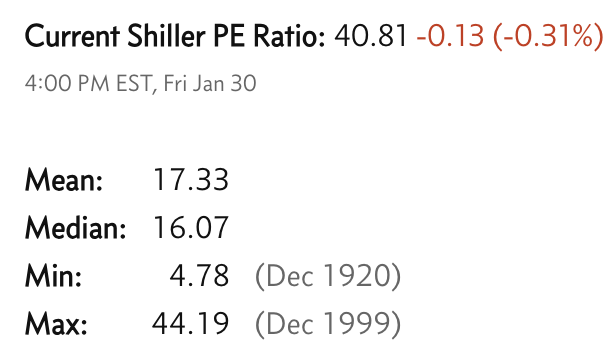

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.