Weekly Market Commentary - Jan 25th, 2025 - Click Here for Past Commentaries

-

While the new administration may be eager for oil companies to increase fossil-fuel production,

the oil and gas companies (and OPEC nations) may not be as keen to do so. Increasing the supply

of oil and gas would ultimately lower energy prices, and in fact put downward pressure on revenue

growth and earnings for major energy producers. Lower energy and gas prices would, however, be

a positive for containing inflation.

Even if U.S. companies were to drill and produce more oil, the logistics of refining may be a headwind

as well. Refineries will not only need to access the drilled oil, but they may need to retool their

facilities to be able to process U.S. oil.

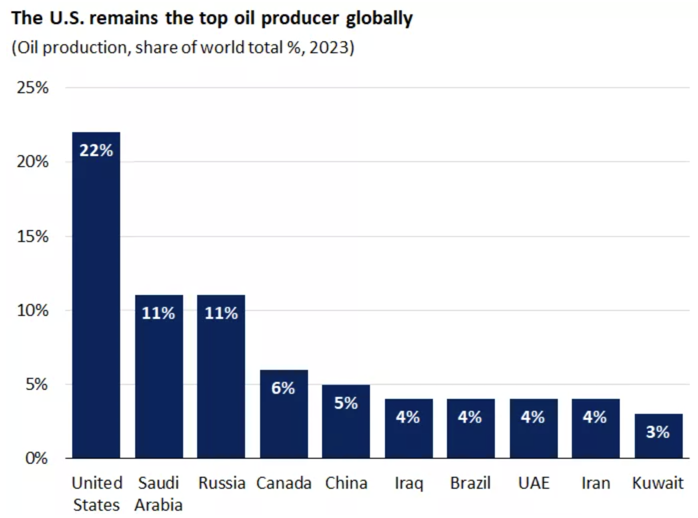

Keep in mind that the U.S. is already a top oil producer globally, but trying to expand this lead further

could bring challenges from both oil companies and refiners globally. Nonetheless, oil and energy prices

have responded thus far, with WTI oil down about 5% since Inauguration Day.

-

The administration seems focused on containing illegal immigration, particularly targeting those

engaged in criminal activity. Investors will be watching to see if the next phase includes broader

deportation activity, which could be more disruptive to labor supply and markets.

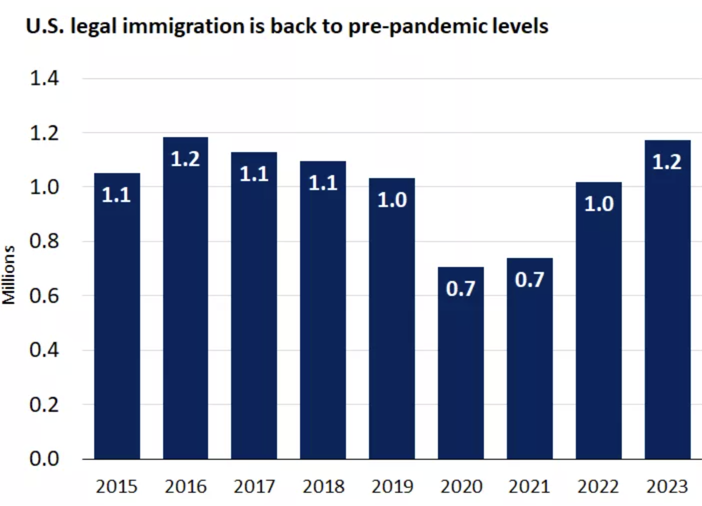

From an economic perspective, the key risk remains that legal immigration declines over time, and

this could weigh on the U.S. labor supply. A smaller labor force could mean not only softer growth

in the U.S., but it may also cause employers to pay higher wages to attract workers, which could

lead to price increases and renewed inflationary pressure. Perhaps the good news is that President

Trump has acknowledged the need for legal immigration into the U.S., especially in areas like

technology that need skilled workers to fill shortages.

-

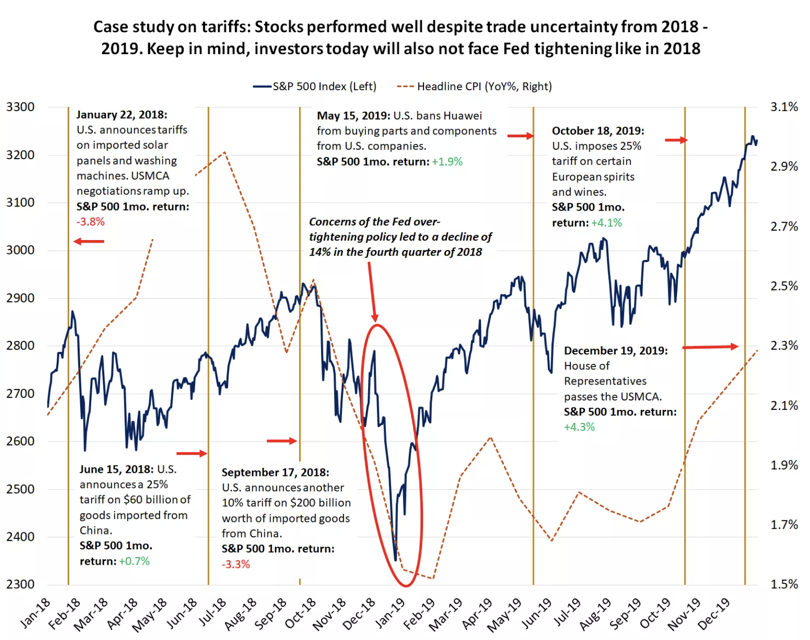

While we certainly expect tariffs are coming (and could spark bouts of volatility), the administration

for now appears to be taking more of a deliberate and research-based approach. In our view, there is

increasing likelihood that tariffs may be targeted to specific sectors and even companies and used more

for negotiating leverage rather than to incite global trade battles. An example of this is President

Trump potentially increasing tariffs against China if it is not willing to make a deal around the social

media giant Tik Tok.

Keep in mind that fighting inflation was a central theme of the Trump campaign. The administration is

likely more sensitive to enacting tariffs that could increase consumer prices and be inflationary or even

perceived to be inflationary. The focus on containing prices in this second Trump term may thus also support

keeping more extreme trade and tariff impulses contained.

-

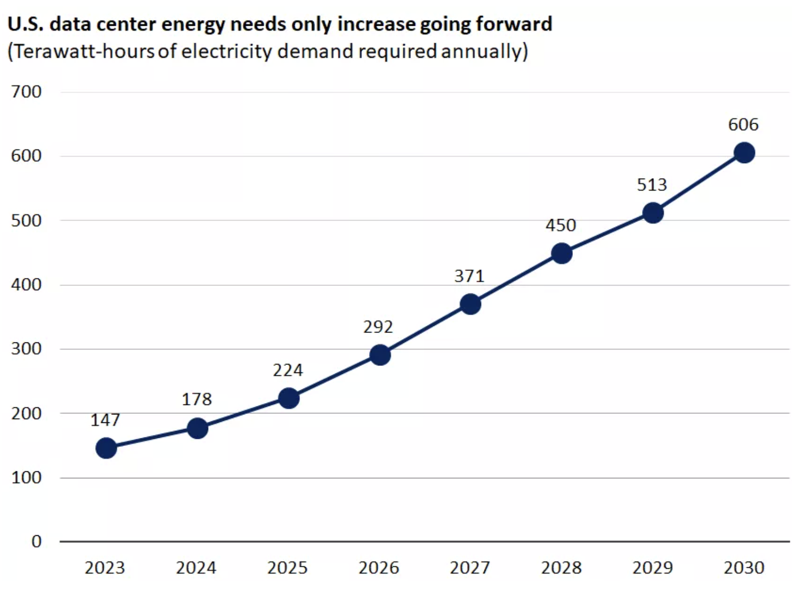

The focus on technology investment is a step in the right direction for the new administration.

The U.S. has already been a leader in AI, with many of the "Magnificent 7" AI infrastructure companies

based in the United States. The investments in data centers and electricity are critical for the U.S.

to maintain leadership and be a driver for AI technology and applications. The government investment

in technology infrastructure, we believe, will pay dividends in the form of enhanced innovation and

productivity in the future.

-

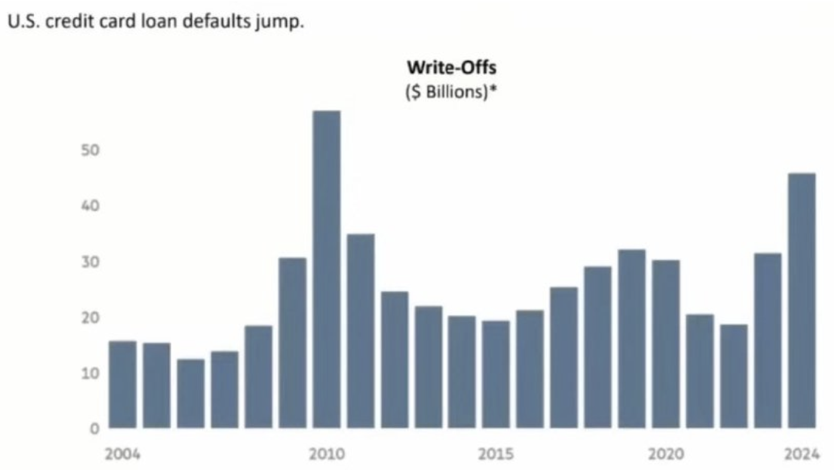

Credit Card defaults hit the highest level since the Great Financial Crisis

-

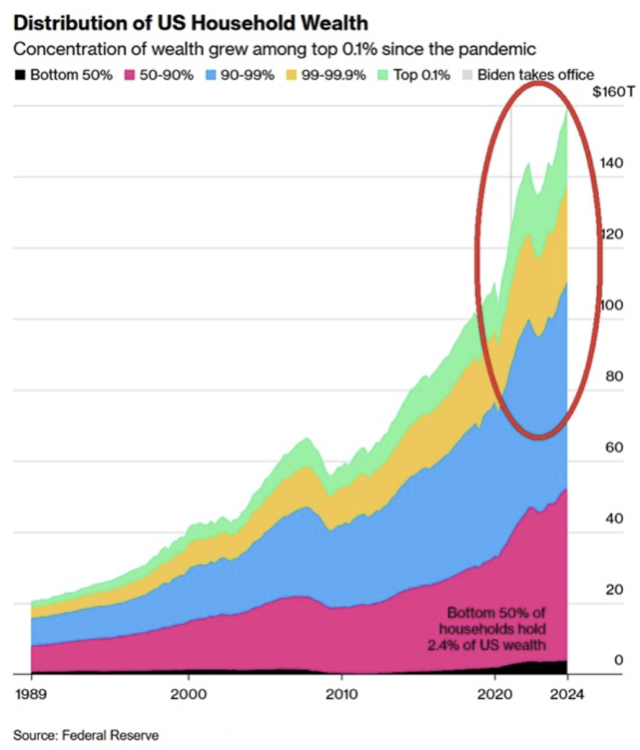

US household net worth has risen ~$56 TRILLION since Q1 2020 and hit a record $160 trillion in Q3 2024.

Currently, the top 10% own $111 trillion of all wealth, accounting for 69% of the total.

The top 0.1% alone own a massive $22 trillion, reflecting 14% of household net worth.

On the other hand, the bottom 50% holds just $3.9 trillion, or 2.4% of wealth.

This comes as the S&P 500 and the Nasdaq 100 have risen 128% and 166% since Q1 2020 while national home

prices have surged ~50%.

-

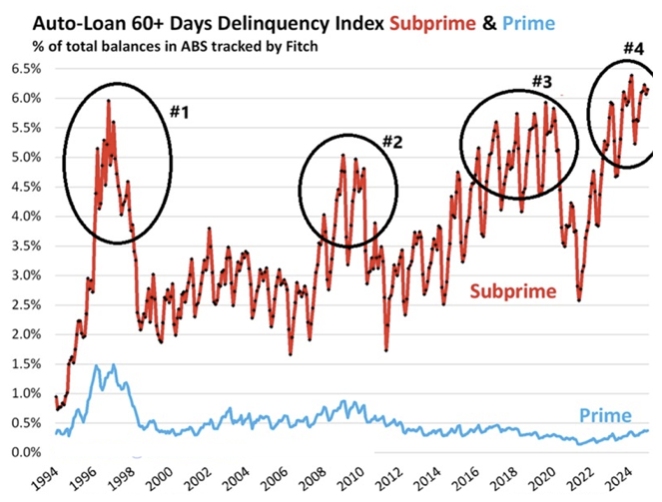

US subprime auto loan 60+ day delinquency rates jumped to 6.2% in December, the highest among any

December on record. Serious delinquency rates have more than doubled over the last 3 years.

The surge accelerated once the Fed began raising rates in March 2022.

Now, delinquency rates have exceeded previous peaks recorded in 1997, the aftermath of the 2008 Financial Crisis, and the 2020 pandemic.

According to Experian, subprime financing accounts for 16.9% of all auto loans as of Q3 2024.

Americans are falling behind on their debt.

-

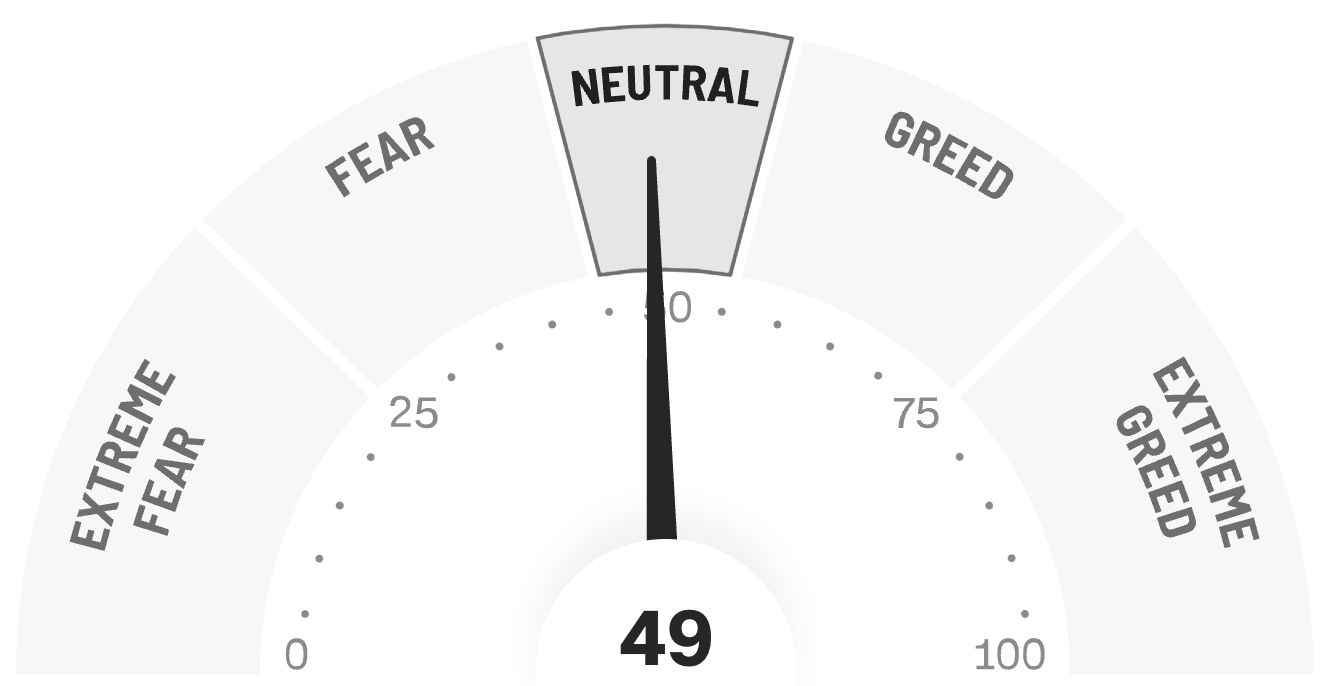

Final Words: Markets are at the all time high and fed is cutting

interest rate, caution warranted. Below is CNN Greed vs Fear Index, pointing at

'Neutral'. This maybe a good time to buy ETF such as VOO.

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

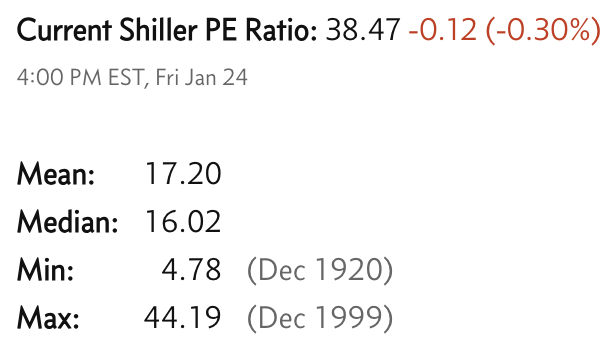

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.