Weekly Market Commentary - Jan 12th, 2025 - Click Here for Past Commentaries

-

This past week, the data confirmed a continuation of this positive economic trend. The

December labor market data in both economies surprised to the upside. Notably, wage gains

continue to outpace inflation rates, a positive for consumers and sentiment.

However, with economic strength improving, the odds of further central-bank rate cuts have

moved lower. As a result, government bond yields moved higher last week, and stock markets

declined. While higher rates may put pressure on valuations and spark some bouts of volatility.

Both economies also face shifts in political regimes in the weeks ahead. In the U.S.,

inauguration day for President-elect Trump is on January 20. All eyes remain on which policies

the new administration will choose to prioritize, including immigration, energy reform, tariffs

and taxes.

-

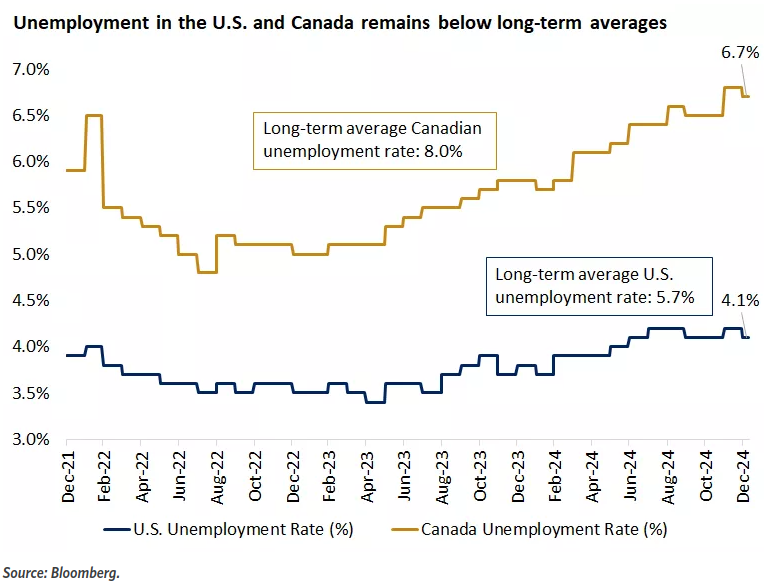

Total net change in jobs for December came in around 91,000, well above expectations of

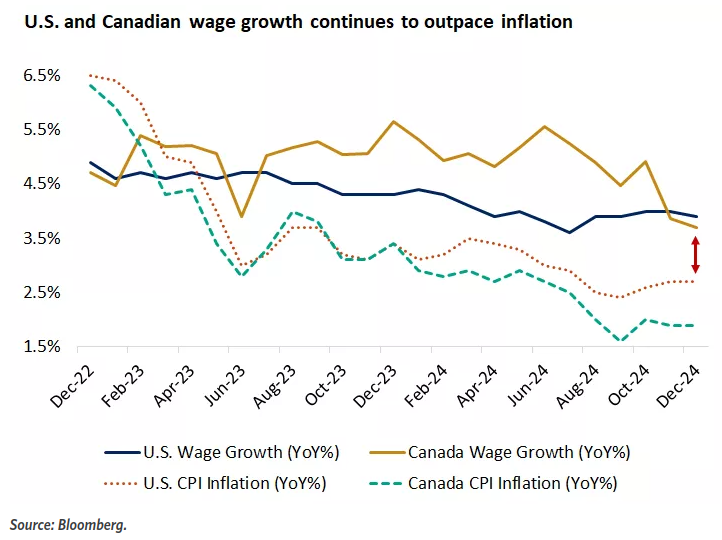

25,000, and the unemployment rate fell to 6.7% from 6.8% last month.* Wage gains in Canada

also eased to 3.7% year-over-year, below estimates of 3.8%, supporting better inflationary

trends broadly. Overall, the employment data points to two key positive trends for economic

growth. First, the unemployment rate in both economies remains benign and well below long-term

historical unemployment rates. This provides a supportive backdrop for both consumers and

businesses to operate. Second, wage gains still exceed the rate of inflation in both the U.S. and

Canada, which means employees are taking home positive real wages. This is supportive of consumer

confidence and spending as well.

-

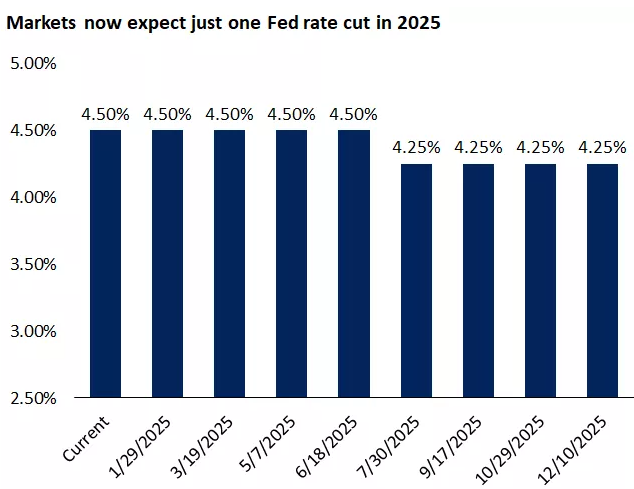

Although the jobs reports were positive, the reaction in the financial markets was largely

negative after this news. This was in part because markets are reassessing the need for further

central-bank rate cuts. In fact, according to the CME FedWatch tool, markets now expect just one

more Fed rate cut in 2025, in the July timeframe, which would bring the fed funds rate to

4.0% - 4.25%. Similarly, the probability of a January rate cut by the Bank of Canada (BoC)

decreased after the jobs data too.

Bond yields moved sharply higher, especially short-term government yields, which tend to be more driven by central-bank policy rates. The higher yields weighed on stocks, particularly those parts of the market with the highest valuations. In the U.S. markets, the technology-heavy Nasdaq underperformed, while defensive parts of the market like utilities and health care held up better. Maintaining a diversified approach to both growth and value investments in portfolios will be an ongoing theme for the year ahead, or just ETF such as VOO.

The uncertainty around which policies are prioritized, and in what order, may continue to remain an overhang on markets. If the administration focuses on some of the more potentially inflationary policies first, like tariffs and immigration reform, this could be more disruptive for markets. However, if these are balanced with pro-growth initiatives like deregulation and tax cuts, we could also see a more balanced outcome in markets. Overall, though, the removal of this policy uncertainty alone may be welcomed by the markets, regardless of the initiatives that are prioritized.

-

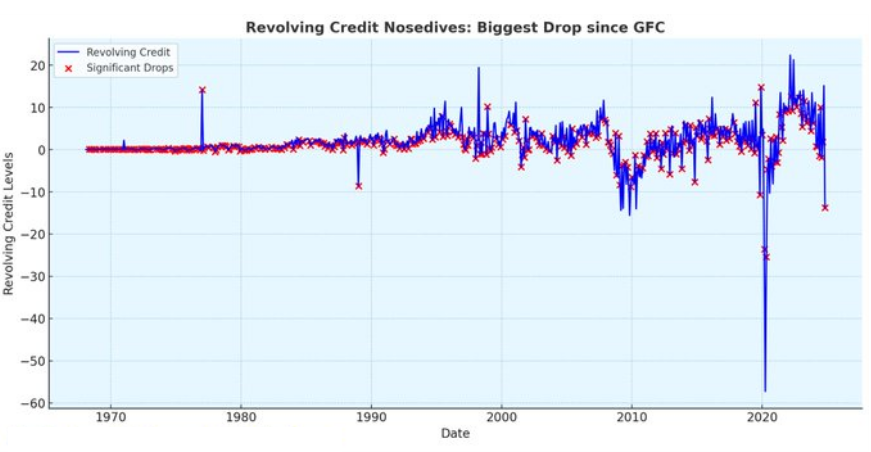

Revolving consumer credit collapsed $7 billion in the month of

November - its largest drop since the Great Financial Crisis,

excluding the pandemic lockdowns

54.5% of US home listings sat on the market for at least 60 days in November without going under contract, the most since 2019.

The share was up 4.6 percentage points from 49.9% in the prior year, marking the 8th-straight monthly increase.

Overall, it took an average of 43 days for a home to go under contract in November, the slowest pace in 5 years.

This development has triggered a sharp surge in active listings.

The total number of homes for sale jumped 12.1% year-over-year in November to the highest level since the 2020 pandemic.

54.5% of US home listings sat on the market for at least 60 days in November without going under contract, the most since 2019.

The share was up 4.6 percentage points from 49.9% in the prior year, marking the 8th-straight monthly increase.

Overall, it took an average of 43 days for a home to go under contract in November, the slowest pace in 5 years.

This development has triggered a sharp surge in active listings.

The total number of homes for sale jumped 12.1% year-over-year in November to the highest level since the 2020 pandemic.

-

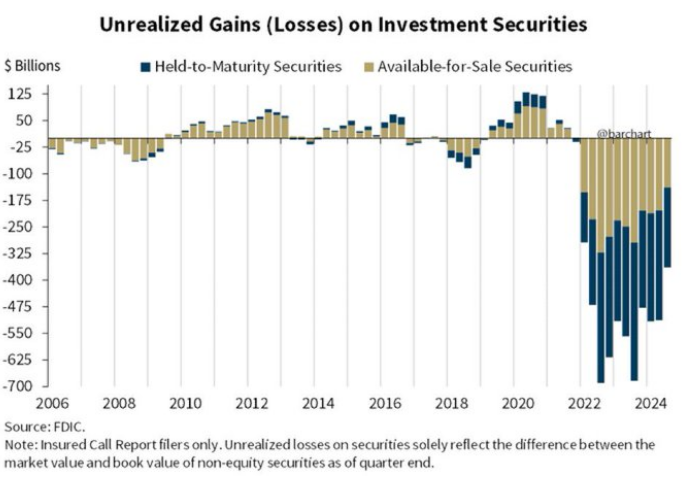

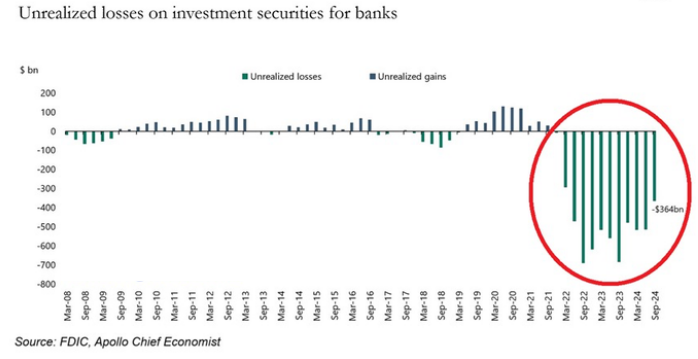

U.S. Banks are currently facing $329 Billion in unrealized losses.

- New ISM data, a key leading indicator for CPI, shows priced paid by purchasing managers are a 22-MONTH high. The last time ISM Prices Paid were this high, inflation in the US was at 6.0%+ in February 2023. Inflation is HOT.

-

Unrealized losses on investment securities for US banks reached $364 billion in Q3 2024.

This is lower than the $513 billion seen in Q2 2024 as interest rates started to gradually decline.

However, banks have now seen 12 straight quarters of unrealized losses, the longest streak since the 2008 Financial Crisis.

Meanwhile, unrealized losses as a % of bank equity capital hit -15% in Q3 2024, up from the low of -34% in Q3 2022.

To put this into perspective, at the 2008 Financial Crisis low, this ratio was much higher, at -6%.

As higher rates return, unrealized losses will follow.

-

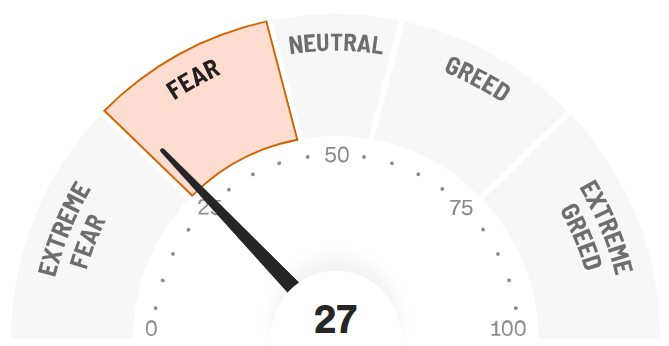

Final Words: Markets are at the all time high and fed is cutting

interest rate, caution warranted. Below is CNN Greed vs Fear Index, pointing at

'fear'. This maybe a good time to buy ETF such as VOO.

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

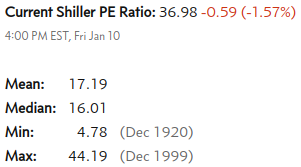

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.