Weekly Market Commentary - Feb 8th, 2025 - Click Here for Past Commentaries

-

The U.S. economy has begun the new year on a healthy note. Despite the myriad headlines and

uncertainty around trade policy ahead, the underlying fundamentals continue to deliver.

After a strong end to 2024, with fourth-quarter GDP growth coming in at 2.3% annualized and

full-year growth at 2.8% year-over-year, first-quarter GDP is on track for above-trend growth

as well. The Fed's GDP-Now tracker is pointing to a robust 2.9% growth rate for the first

quarter, well above trend rates of 1.5% to 2.0%.

In addition, the consumer continues to show signs of strength. As we know, consumption makes

up about 68% of GDP in the U.S., and households thus far continue to spend on both goods and

services. Consumption grew by 4.2% in the fourth quarter of 2024, well above long-term averages of

about 3%, and at the highest growth rate of the year.

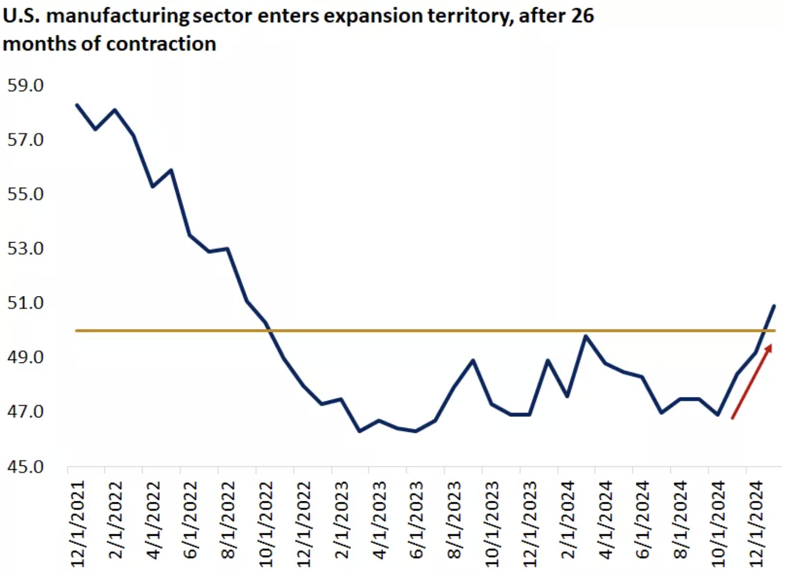

Finally, the manufacturing economy in the U.S. is also starting to show signs of life.

The U.S. manufacturing PMI, a gauge of business activity in the manufacturing sector,

has flipped to indicate expansion for the first time since 2022. While the services sector

has been stronger, manufacturing had remained sluggish in the post-pandemic period and

now is perhaps starting to show improvement and better momentum heading into 2025.

-

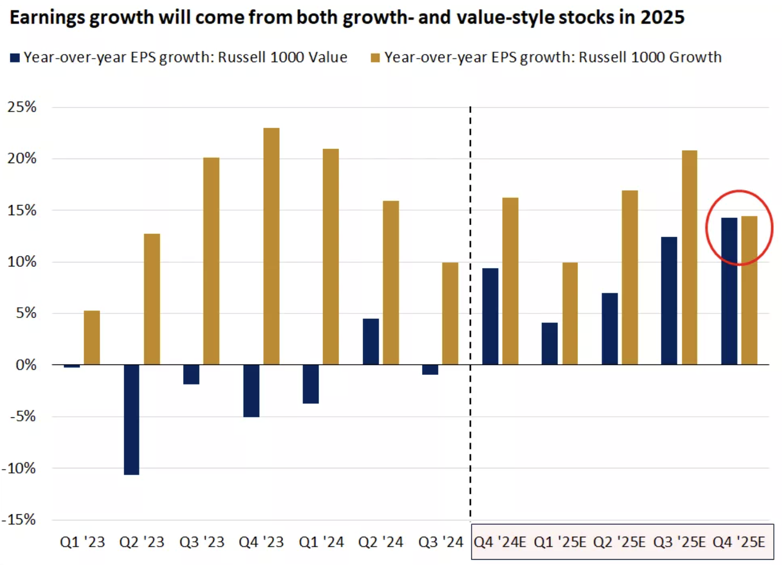

One of the biggest drivers of underlying stock-market performance is the direction of

corporate earnings. In our view, earnings for 2025 remains on track for 10%-15% growth

year-over-year, the highest level since 2021.1 We expect both growth and value parts

of the market to contribute to earnings growth this year, which also supports the

ongoing broadening of sector leadership in the stock market.

The fourth quarter 2024 earnings season is underway now, and corporate earnings continue to surpass forecasts. About 60% of S&P 500 companies have reported earnings already, and among these, 77% have exceeded expectations. This is above the 10-year average of 75% and in line with the five-year average of 77%. While there have been some high-profile misses and a focus on capital spending, particularly among the mega-cap technology stocks, the overall direction continues to support corporate earnings momentum heading into 2025. As we look toward the back half of this year, corporations will be paying particular attention to policy updates on corporate tax rates and deregulation. If the new administration can maintain or lower current tax policy, and loosen regulations broadly, this would generally be viewed favorably across sectors and could be a driver of positive market sentiment.

-

Finally, the January nonfarm-jobs report in the U.S. pointed to a labor market that continues to

hold up well. Keep in mind that when households feel confident in their jobs and the job market

broadly, they are more inclined to consume.

The labor market has continued to be a source of strength for the U.S. economy, and the latest

jobs report was no exception. The total jobs added came in at 143,000, modestly below expectations

of 175,000. However, the last two months of job gains were revised higher, bringing the three-month

average to a healthy 241,000, above the 165,000 average over the last 12 months.

The unemployment rate in the U.S. fell to 4.0%, below expectations of 4.1% and last month's 4.1%

reading, and remains well below the long-term U.S. average of 5.7%.

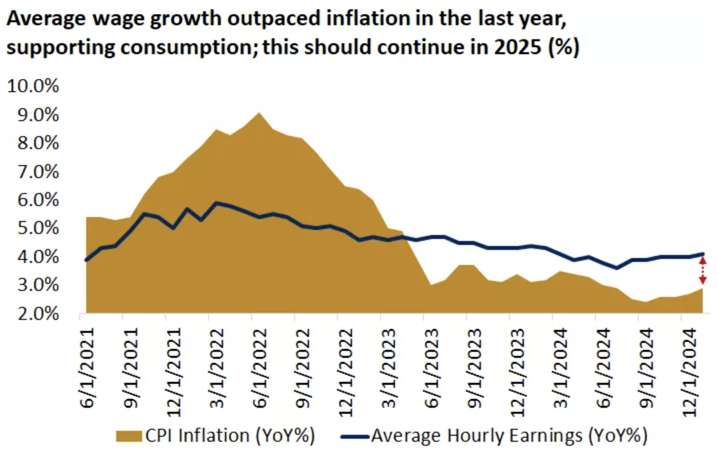

One area to watch is the average hourly earnings, or wage growth, component of the labor market.

This ticked higher to 4.1% year-over-year, above expectations of 3.8%. The elevated wage gains

could put upward pressure on services inflation, supporting the case for the Federal Reserve to

remain on hold with rate cuts for now.

On the other hand, better wage growth is also supportive of households and consumption. Wage

gains have been outpacing the rate of inflation since mid-2023, which helps employees bring

home positive real wage gains and should support better consumer confidence overall.

-

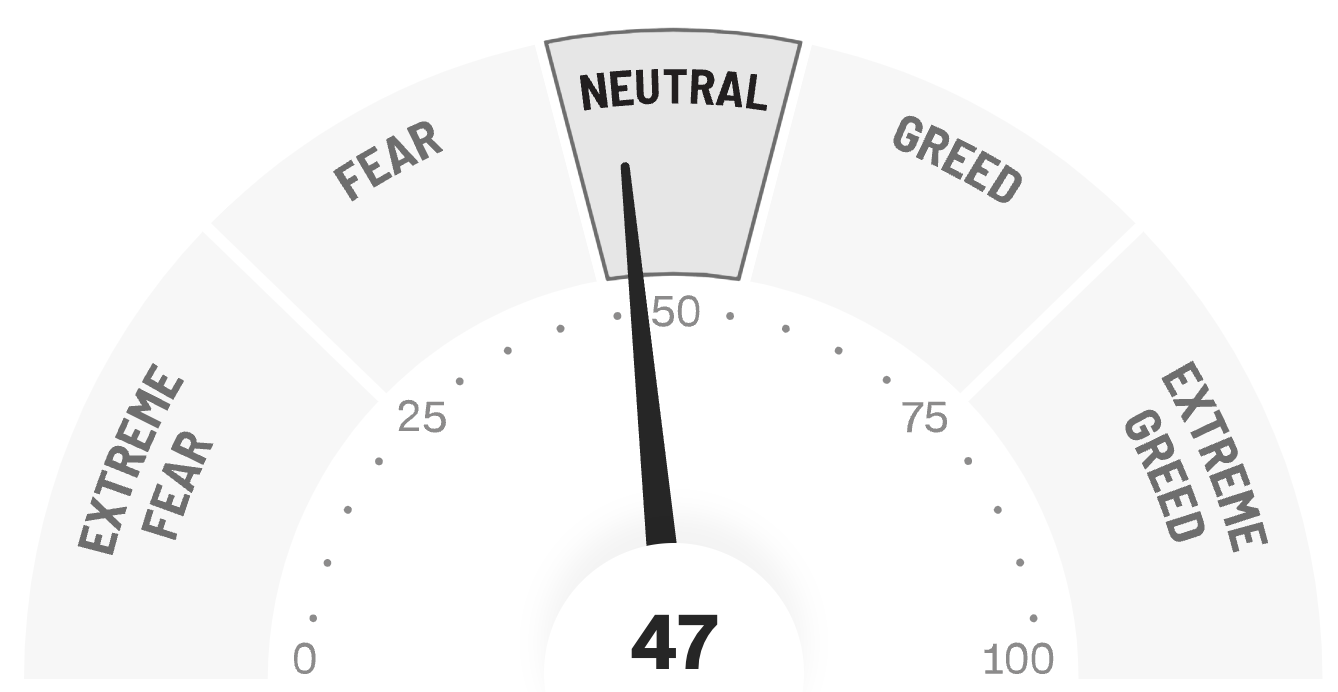

Final Words: Markets are at the all time high and fed is cutting

interest rate, caution warranted. Below is CNN Greed vs Fear Index, pointing at

'Neutral'.

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

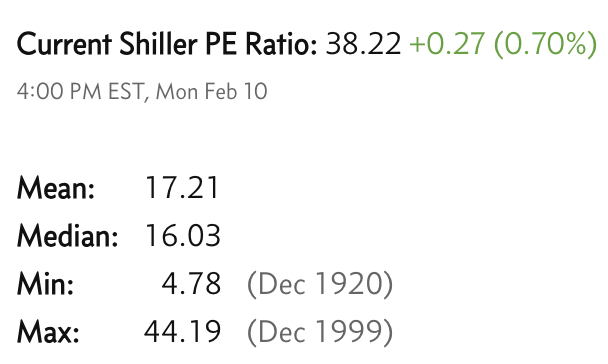

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.