Weekly Market Commentary - Feb 22th, 2025 - Click Here for Past Commentaries

-

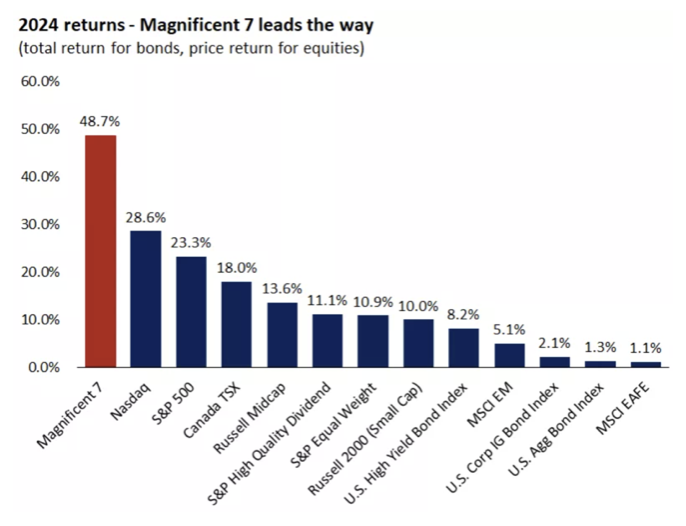

In 2024, the mega-cap technology stocks led broader stock markets, particularly in the

first half of last year. The technology-heavy Nasdaq and the "Magnificent 7"1 stocks, which

are considered the leaders of the artificial intelligence (AI) trade, sharply outperformed

the market in 2024 and drove over 50% of the S&P 500 returns.* This year, the performance

of these stocks has been mixed, with only two of the seven Mag-7 stocks outperforming the

S&P 500, and with the group lagging behind most other asset class returns.

Stocks include AAPL, AMZN, GOOGL, META, MSFT, NVDA, TSLA

The mega-cap technology trade remained somewhat vulnerable heading into 2025. After the Magnificent 7 returned over 150% in 2023 and 2024, valuations on these stocks were extended, although perhaps not to the same degree as the 1999 Tech Bubble, given that earnings growth has been robust for most of these companies.

In addition to valuation concerns, these are global companies that may be more exposed to tariff and trade uncertainty, especially in the semiconductor and hardware space.

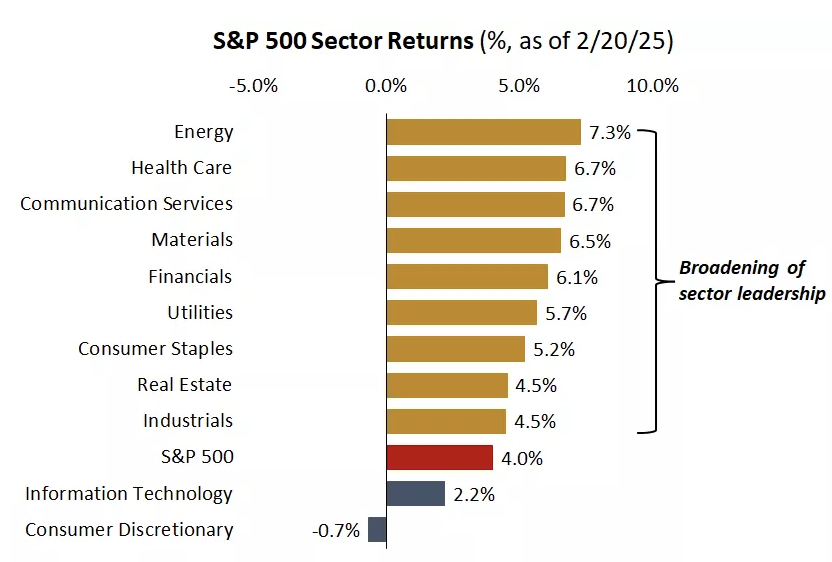

Finally, earnings growth in 2025 is expected to be more balanced. Both tech and non-tech sectors are expected to contribute to earnings growth, which supports a broader set of market leadership.

This has played out thus far in 2025, with 10 of the 11 S&P 500 sectors positive for the year, and with areas like financials, energy and health care outperforming, while technology and consumer discretionary have lagged. In our view, this broadening theme has legs, and we continue to favor both large-cap and mid-cap stocks across growth and value sectors.

-

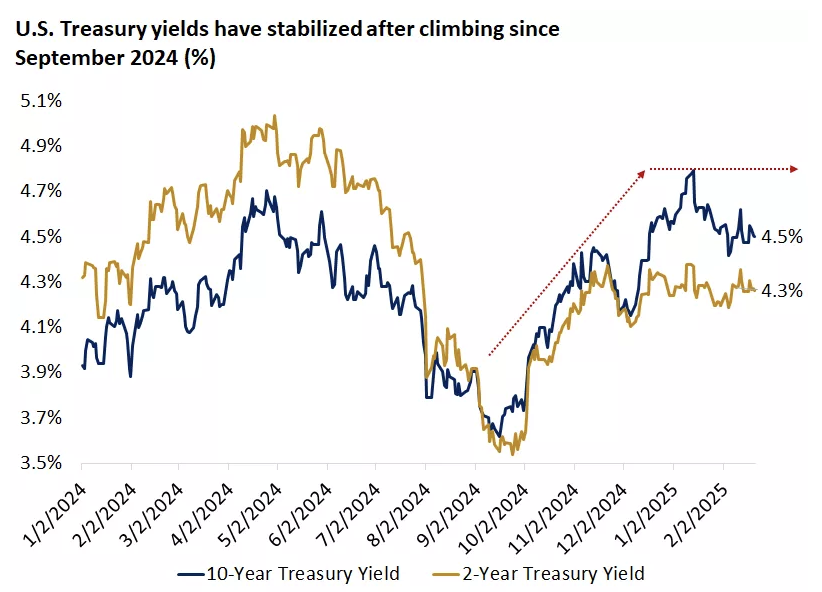

The U.S. 10-year Treasury yield rapidly rose by nearly 120 basis points (1.2%), from about 3.6% to 4.8%,

from September to early January. This sharp move higher was driven by a combination of better-than-expected

U.S. economic data, uncertainty around inflation and spending by the new administration, and the idea that

the Federal Reserve would likely not be cutting interest rates much further in 2025. Over the past few weeks,

however, Treasury yields have stabilized, and the 10-year yield has returned to around 4.5%.

-

We see a few reasons why yields have now stabilized and returned to around 4.5%. First, despite concerns,

inflation data thus far has been generally contained. In fact, we will be getting personal consumption

expenditures (PCE) inflation data next week, which is often considered the Fed's preferred inflation

gauge, and the expectation is for the headline inflation rate to moderate from 2.6% to 2.5%. While

this is still above the Fed's 2.0% target, it is well below recent highs of over 7.0% inflation.

Second, the new administration continues to focus on cost cutting, with a particular eye toward the federal government, and markets may see this as a reversal from recent deficit spending. This could also help keep Treasury yields contained.

Finally, there have been growth concerns that have been creeping up in recent data points. Retail sales for January came in below expectations, bellwether consumer companies like Walmart have been giving soft guidance, and the potential for tariffs may weigh on consumption. Not only does the prospect of moderating economic growth weigh on bond yields, but it also puts the idea of Fed rate cuts back on the table.

In our view, if the economy or labor market slows in the quarters ahead, the Fed will likely start to consider one or two rate cuts for the remainder of this cycle, which would be supportive of stock and bond markets. More broadly, we believe Treasury yields will likely remain range-bound, with the 10-year in the 4% to 4.5% range for much of the year.

-

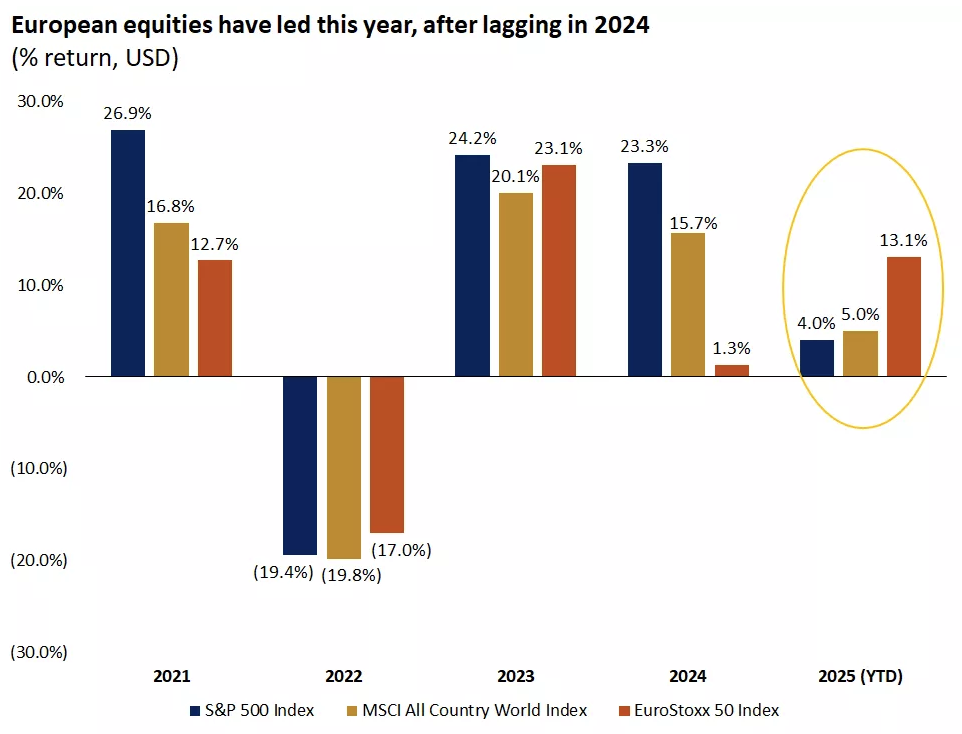

Perhaps one of the most interesting trends of 2025 thus far has been the outperformance of

European stock markets versus most of the globe. The EuroStoxx 50 index is up about 13% this year,

compared with the S&P 500 up 4% and the MSCI World Index up about 5%. This comes after its notable

underperformance versus the U.S. and global markets last year.

-

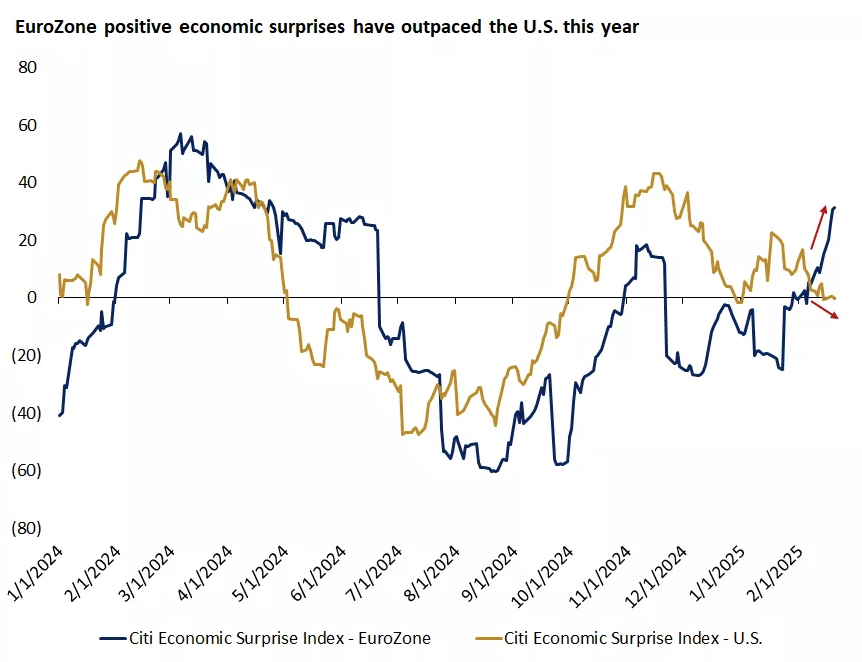

We believe the outperformance of European equities has been driven by a few key reasons. First,

we are seeing European markets rally as the U.S. dollar has come down from recent highs, which

is supportive of international stocks and sentiment. We have also recently seen more positive

economic surprises coming out of the eurozone than in the U.S.

-

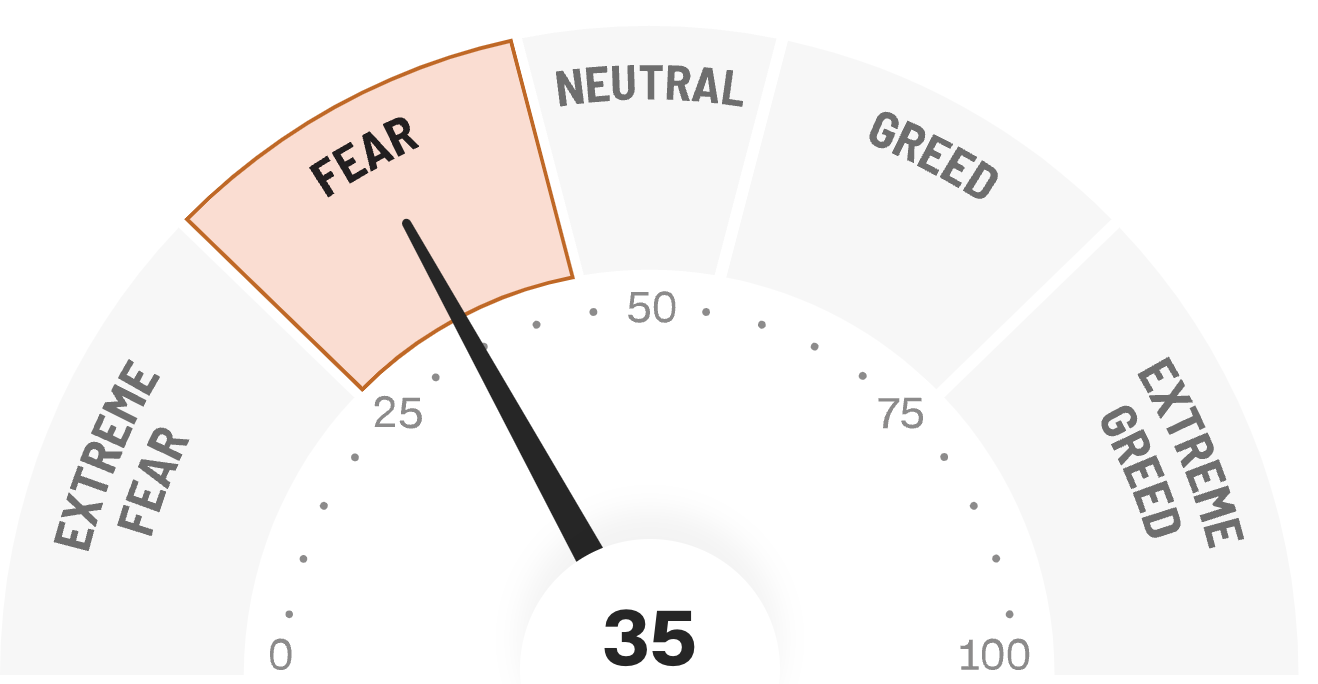

Final Words: Markets are at the all time high and fed is cutting

interest rate, caution warranted. Below is CNN Greed vs Fear Index, pointing at

'Neutral'.

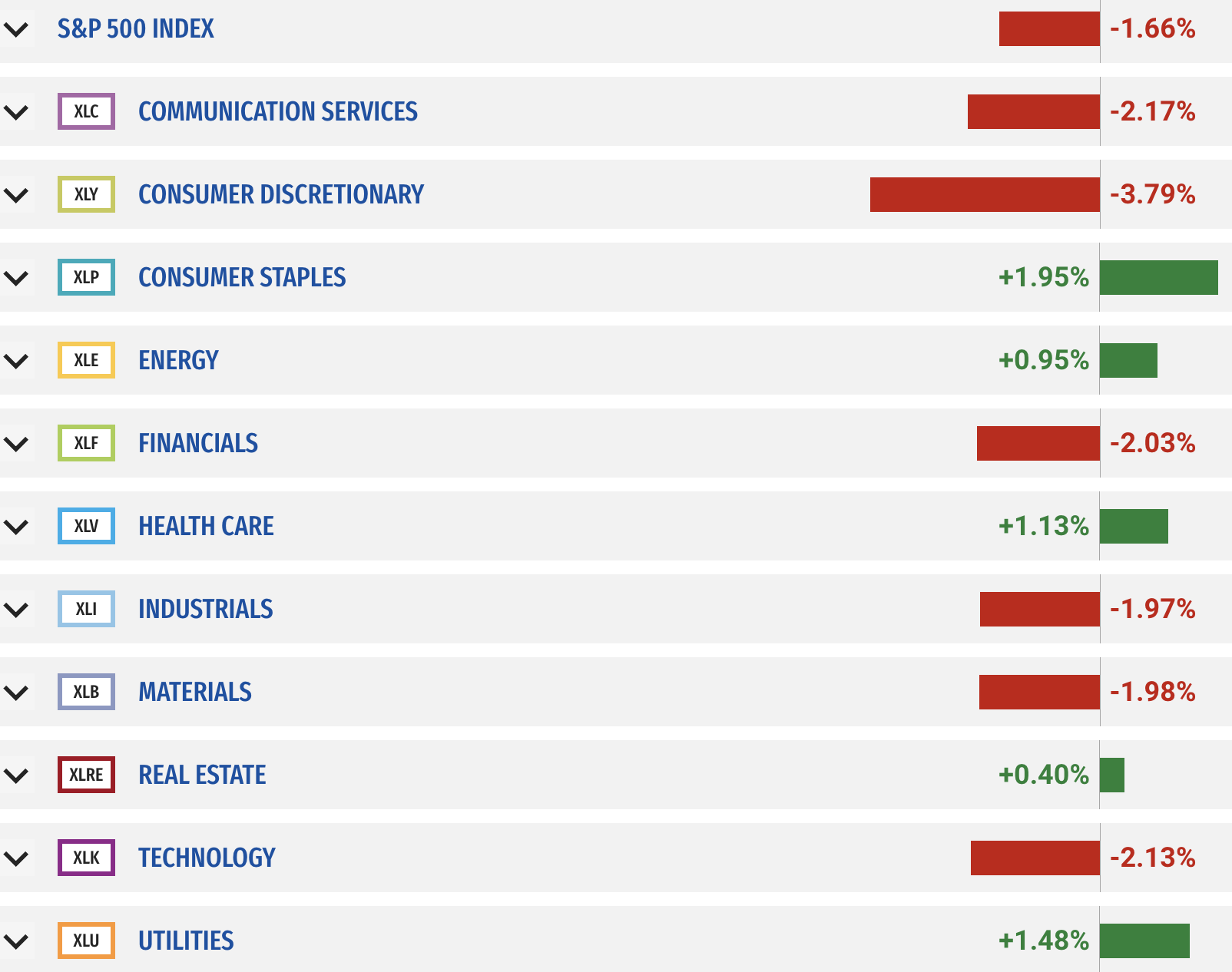

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

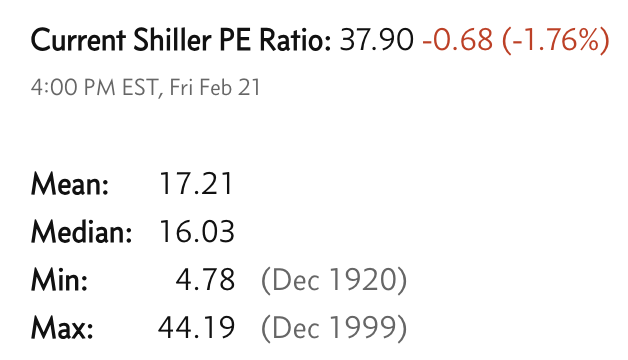

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.