Weekly Market Commentary - Feb 1st, 2025 - Click Here for Past Commentaries

-

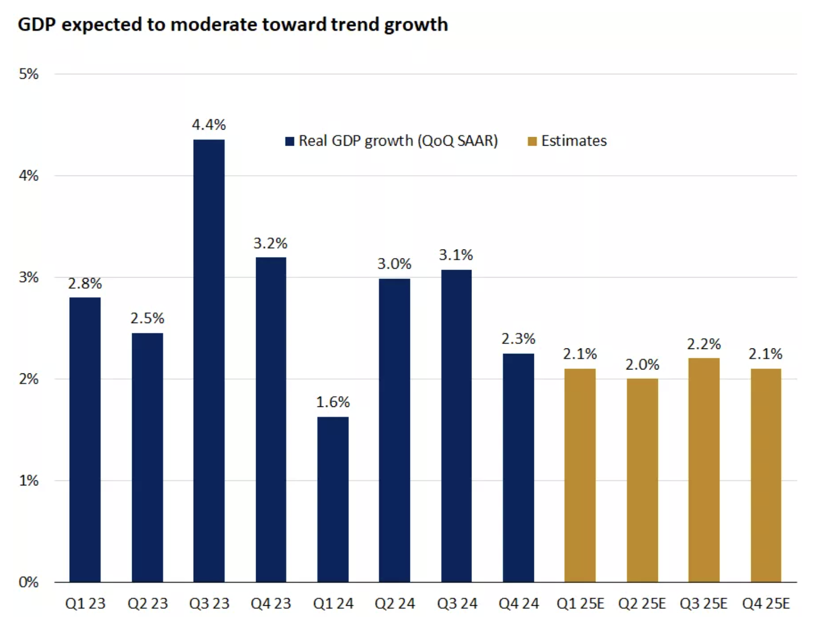

Fourth-quarter real GDP showed the U.S. economy remains on strong footing, growing 2.3% annualized,

slightly below forecasts calling for 2.4%. Consumer spending, representing about 68% of the economy,

was the main driver of the expansion, rising at a 4.2% annualized rate, the highest reading since the

first quarter of 20231. Downturns in investment and exports were the primary detractors, contributing

to the decline in real GDP growth from the prior quarter. For the year, real GDP grew by 2.8% in 2024,

down from 2.9% in 2023.

In our view, with the unemployment rate at 4.1% and job openings exceeding unemployment, a healthy labor market should keep wage gains above inflation, providing positive real wages. In addition, the U.S. manufacturing sector, which remained in contraction for much of the past two years, showed signs of stabilizing this month. We expect the healthy labor market and positive real wages to support consumer spending, which, combined with a potentially stabilizing manufacturing sector, should continue the economy's momentum this year.

While growth could cool in the first half of the year as consumers, particularly those in lower income brackets, potentially pull back on discretionary spending, we don't expect a recession. We see the potential for growth to reaccelerate in the back half of the year, driven by Fed interest-rate cuts and pro-growth policies, such as deregulation and tax cuts.

-

Corporate earnings ramped up this week, with four of the "Magnificent 7" companies reporting.

Apple, Microsoft and Meta delivered strong results, above estimates for both earnings per share

and revenue, while Tesla missed on both measures. Despite disappointing results, Tesla shares

traded higher on optimism over the favorable regulatory environment, new more affordable models,

and autonomous vehicles, including Robotaxi.

Technology stocks are down this week but have rebounded from Monday's sharp sell-off that was sparked by Chinese AI startup DeepSeek. The company's AI model reportedly performs comparably to those of leading U.S. technology companies, despite being developed at a fraction of the cost and requiring less computing power. While DeepSeek's development and true costs are still to be verified, it has raised questions as to whether leading U.S. AI companies may be overspending and need to be more efficient. Despite the concerns around the competition coming from Chinese companies like DeepSeek, we continue to see U.S. technology firms remaining leaders of the global AI market, benefiting from deep financial resources, talent and technology to drive innovation. We expect these companies to respond to this competitive threat, especially considering DeepSeek's AI model is open-source. This means the programming and coding behind its performance is transparent and openly available, potentially allowing competitors to incorporate any enhancements to improve their own AI models. Enhanced performance, lower development costs, and reduced computing-power demands should lead to further adoption of AI among businesses and consumers, potentially driving more investment in the space.

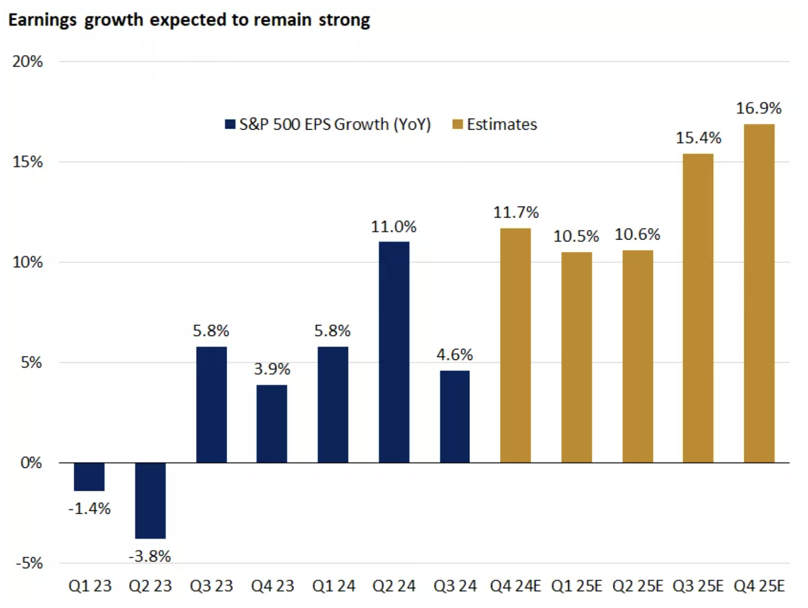

For the quarter, S&P 500 earnings are on track to grow roughly 12%, which, if achieved, would be the strongest pace since 2021. Earnings growth is expected to be broad as well, with seven of the 11 sectors forecast to report higher earnings. Strong earnings momentum is expected to carry over into 2025, with estimates calling for earnings growth of more than 14%1. In our view, healthy economic conditions and the potential for deregulation should drive strong earnings growth this year, helping sustain the bull market.

Broadening earnings growth has contributed to a rotation in market leadership. Over the past six months, the financial and industrial sectors have each outperformed the technology sector. Looking at more recent performance, the S&P 500 is off to a strong start this year, up about 3.9%, while the technology sector is down 1.1%. We expect market performance to continue to widen beyond technology-focused stocks like the Magnificent 7.

-

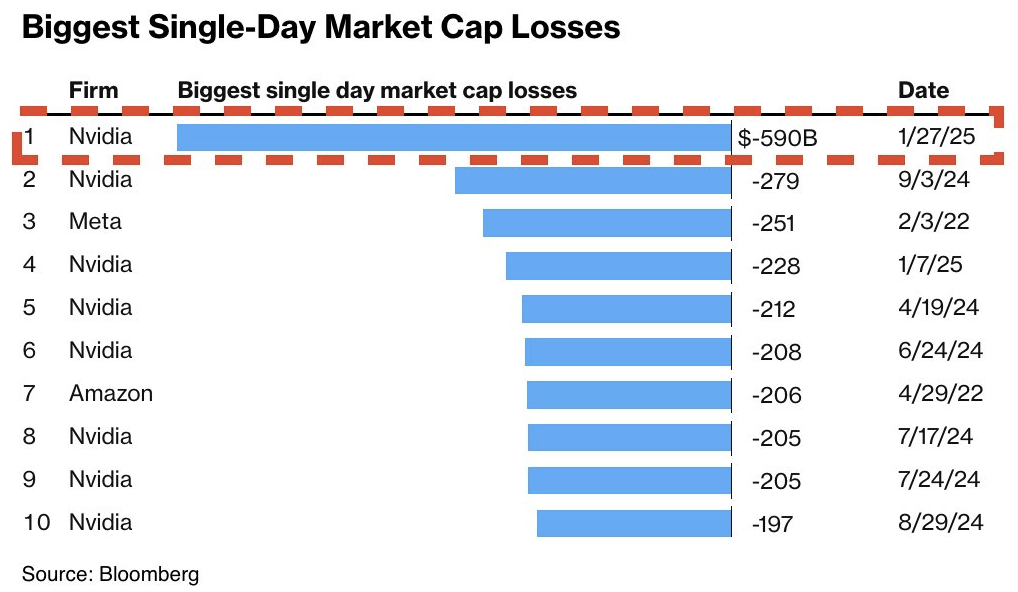

On Jan 27th 2025, Nvidia, closes the day down -17%, officially erasing -$590 BILLION of market cap.

This marks the largest 1-day loss of market cap in a single stock in history, and it's not even close.

- A record number of consumers are making minimum credit cards payments, per CNBC. The share of active credit card holders just making minimum payments rose to 10.75% in the third quarter of 2024, the highest ever in data going back to 2012.

-

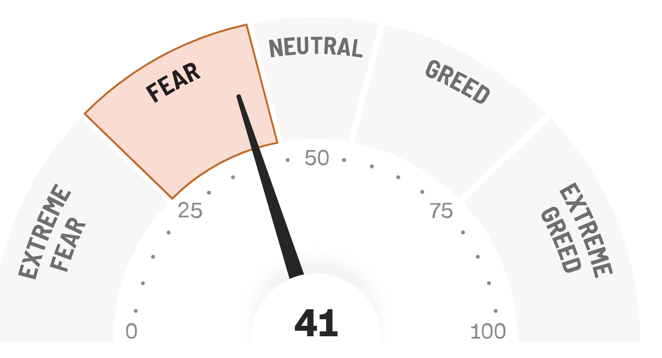

Final Words: Markets are at the all time high and fed is cutting

interest rate, caution warranted. Below is CNN Greed vs Fear Index, pointing at

'Neutral'. This maybe a good time to buy ETF such as VOO.

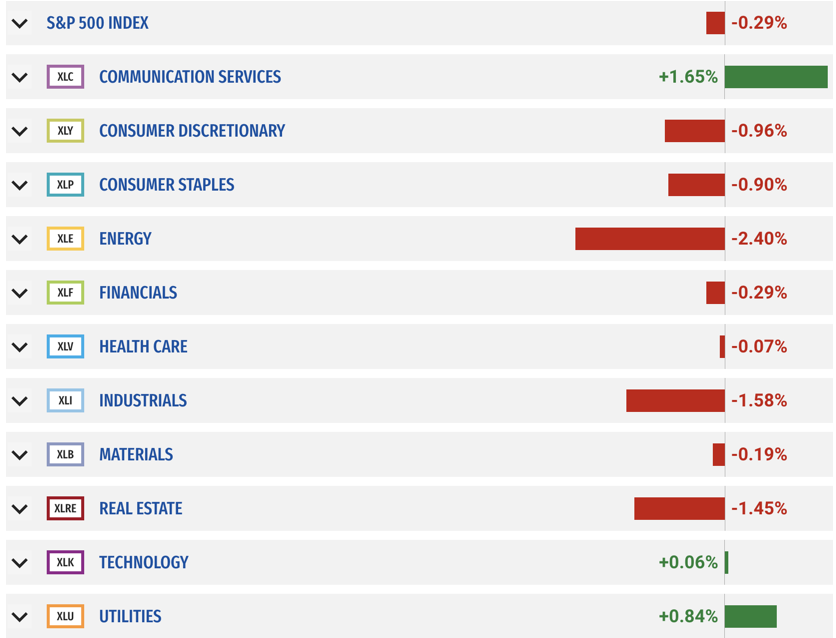

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.