Weekly Market Commentary - Dec 28th, 2024 - Click Here for Past Commentaries

-

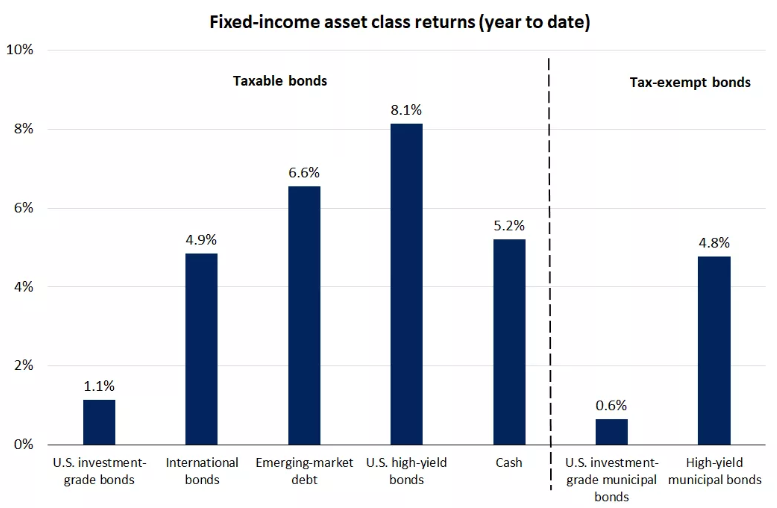

Fixed-income returns varied widely by asset class this year, demonstrating the value

of diversification. Allocations beyond U.S. investment-grade bonds offered the opportunity

to enhance performance. Bonds appear to be well-positioned to deliver income and

diversification as we begin 2025, as central banks continue easing monetary policy toward a

neutral stance, normalizing yields and potentially reducing interest rate volatility.

We expect the Fed to slow the pace of rate cuts, targeting the 3.5%-4% range.

U.S. investment-grade bond yields appear likely to retake the lead over cash, supported by a

yield advantage.

-

In 2024, fixed-income investments delivered wide-ranging returns amid elevated interest

rate volatility as markets adjusted expectations for inflation and Federal Reserve interest

rate cuts. Key investment return drivers impacted major asset classes differently, offering

the opportunity to enhance performance by diversifying beyond U.S. investment-grade bonds.

As we begin 2025, bonds appear to be well-positioned to deliver their key benefits of income

and diversification as central banks ease monetary policy toward a neutral stance, though at a

slower pace, normalizing yields and potentially reducing interest rate volatility.

-

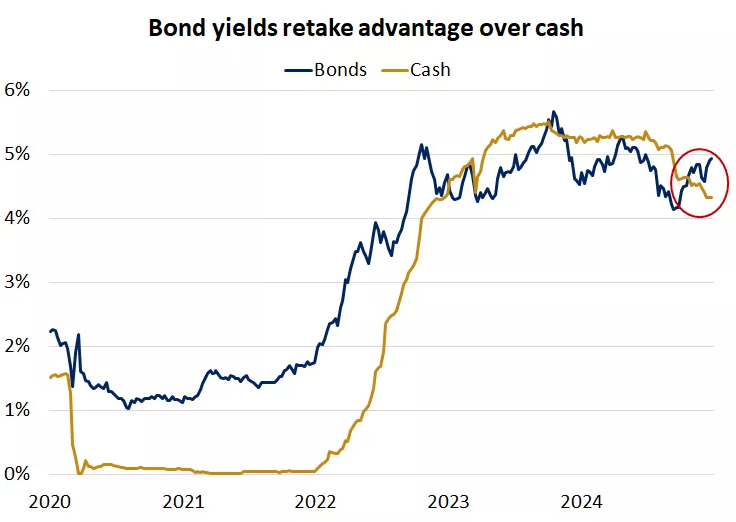

While the backup in bond yields over the past few months has impacted bond prices, it also sets

the stage for stronger performance ahead as yields are typically the key driver of fixed-income

returns. Fed rate cuts have driven cash yields below bond yields. Further Fed rate cuts could cause

cash yields to fall more than intermediate- and long-term bond yields, likely steepening the yield

curve and widening the yield advantage of bonds over cash.

Over the past few years, many investors have gravitated toward cash and cash-like instruments,

such as money market funds and CDs, as these investments offered favorable yields. While cash can

provide important benefits, holding too much in cash or cash-like investments can present risks,

such as the potential for lower returns over the long term. For perspective, since 1981, cash has

generated annualized returns of 4.1%, compared with 6.8% for U.S. investment-grade bonds.

-

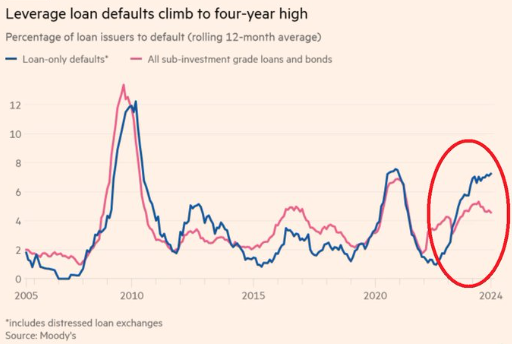

US firms are defaulting on junk loans at the fastest pace since the 2020 CRISIS.

This comes as firms took MASSIVELY on debt during the low rates environment in 2020 and

now are paying the price.

-

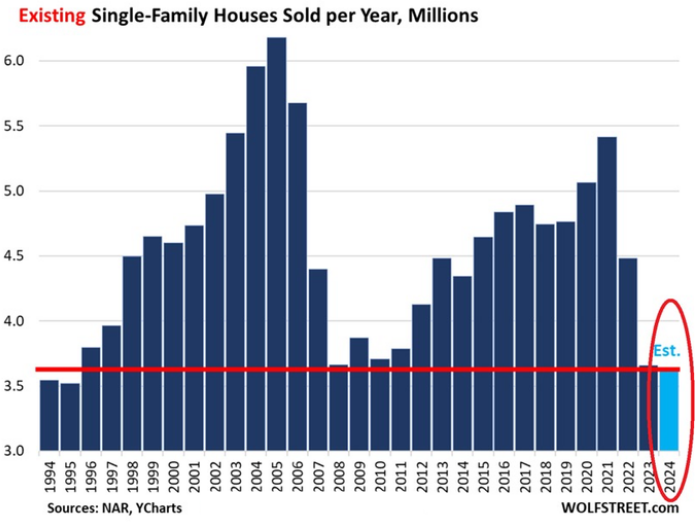

US existing home sales are set to close at 4.04 million in 2024, marking the worst year since 1995.

Sales are set to be even lower than during the 2008 Financial Crisis.

The lack of demand for existing homes comes as home prices have jumped over 50% since 2020.

Over the same time period, mortgage rates have nearly TRIPLED, making affordability even worse.

The average rate on a 30-year mortgage is up 100 basis points since September alone, to 7.1%,

despite the Fed cutting rates by 100 basis points.

-

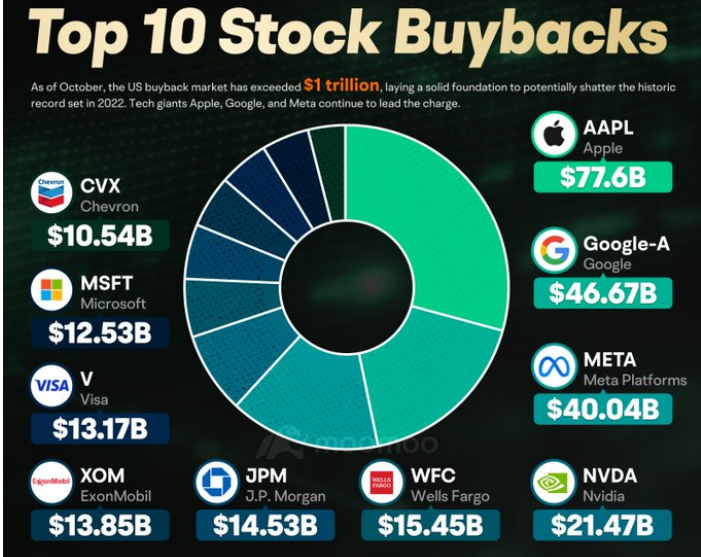

The US stock market is becoming even more concentrated:

The top 10 stocks now reflect a record 40% of the S&P 500's market cap.

This percentage now exceeds the 2000 Dot-Com bubble levels by ~14 percentage points.

In 2024, these stocks have added over $7 TRILLION in market cap and are now worth a record $20.9 trillion.

To put this into perspective, the entire European stock market is worth ~$16 trillion, or $4.9 trillion LESS.

-

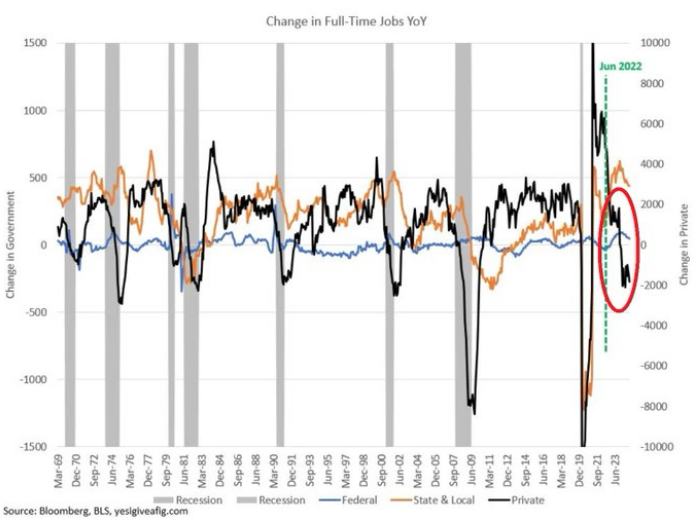

US private sector full-time jobs have DROPPED by nearly 2 MILLION over the past year.

Such a drop has never happened outside of recessions.

The only gain in full-time jobs has been in the government sector.

Job market is weak

-

Stock buybacks is mostly the reason for top stocks to perform so well in 2024.

Apple brought more than 70 billion in their own stock, leading the pack. Diminishing sales

can be countered by buying back stocks ? New economy.

-

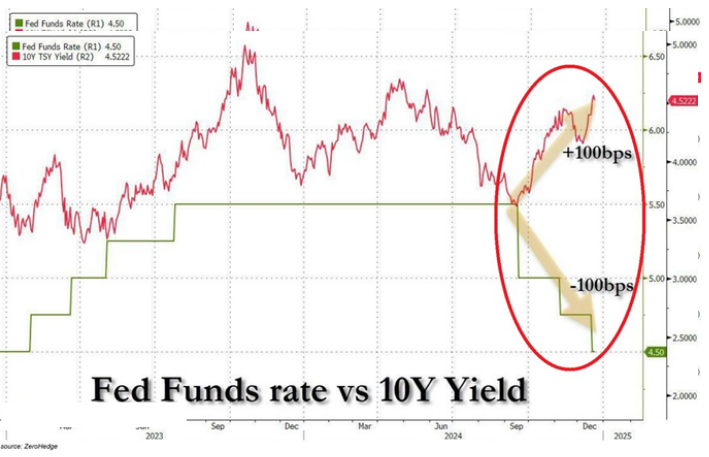

Treasury yields are soaring as the Fed cuts rates:

The Fed has cut rates by 100 basis points this year, from 5.50% to 4.50%.

Meanwhile, the 10-year Treasury yield has SURGED by 100 basis points since September to

a 6-month high.

This comes as inflation is officially back on the rise.

The Fed itself has raised its PCE inflation forecast to 2.5% in 2025, up from 2.1% in September.

The central bank now expects the inflation rate to come down to its 2% target in 2027 instead of

2026 as previously projected.

-

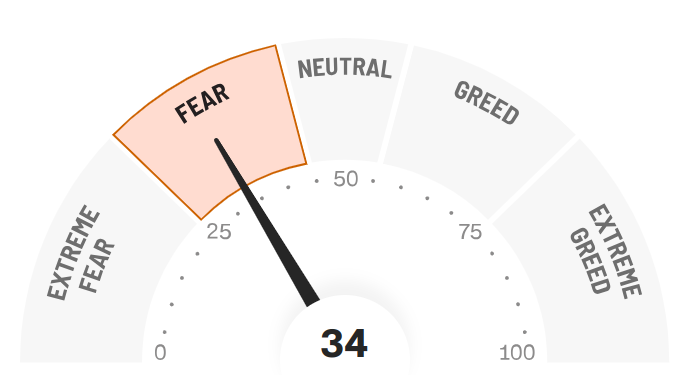

Final Words: Markets are at the all time high and fed is cutting

interest rate, caution warranted. Below is CNN Greed vs Fear Index, pointing at

'fear'. This maybe a good time to buy ETF such as VOO.

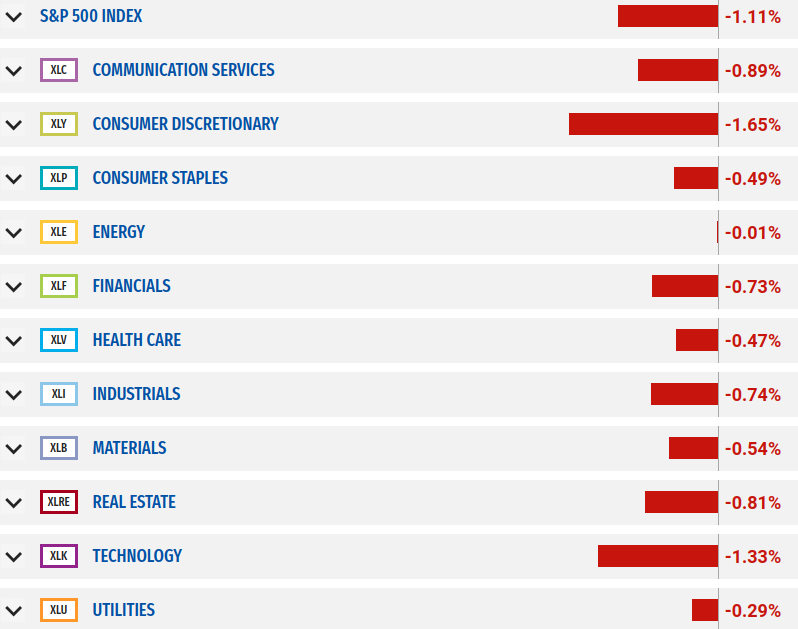

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

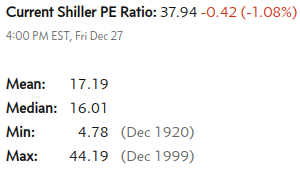

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.