Weekly Market Commentary - Dec 21st, 2024 - Click Here for Past Commentaries

-

The Fed delivers a modestly hawkish outlook at its final meeting of 2024

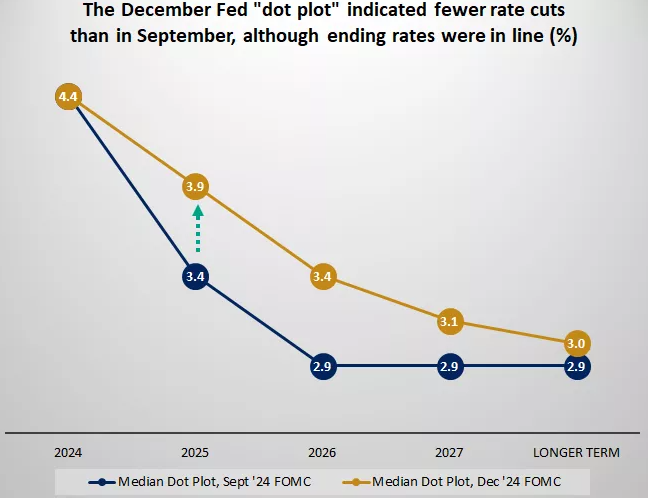

Overall, the December FOMC meeting pointed to a Fed that wanted to proceed with a bit more

caution on the path of rate cuts. The Fed cut rates by 0.25% to 4.25% - 4.5%, but its dot plot

indicated just two rate cuts in 2025, versus four rate cuts penciled in at the September

FOMC meeting.

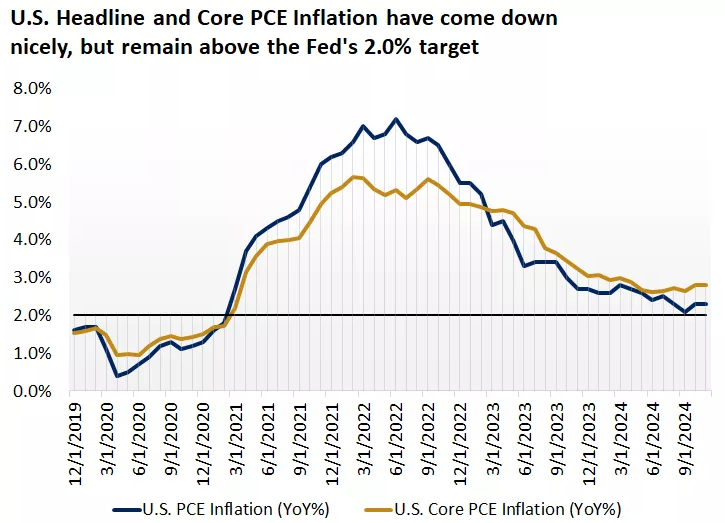

The Fed has already cut rates by one full percentage point, from 5.5% to 4.5%, which has brought them meaningfully closer to a more neutral rate. The Fed noted that inflation has come down substantially in the last two years but still remains elevated versus its 2.0% target. The Fed continues to see inflation moderating, but at a slower pace. Its updated projections now show core personal consumption expenditure (PCE) inflation falling to 2.0% by 2027. Powell alluded briefly to potential changes in trade and tariff policies, which could have an impact on inflation as well. However, he also noted that there are still too many unknowns around the new policies to make a definitive conclusion on inflation estimates. We believe the Fed's more cautious approach to rate cuts are somewhat warranted, given that inflation remains above 2.0% and that there are uncertainties over tariff policies. However, the direction of interest rates is lower over the next 12 months. This should be supportive for both consumption and household and corporate borrowing costs. In addition, markets had already been pricing in just two rate cuts for 2025, so the Fed's updated dot plot brings it in line with market expectations, though markets are now pricing in just one Fed cut in 2025, according to CME FedWatch tool. In our view, with this reset in market expectations, the Fed now has more room to surprise markets with more cuts than anticipated, which could support market sentiment as well.

-

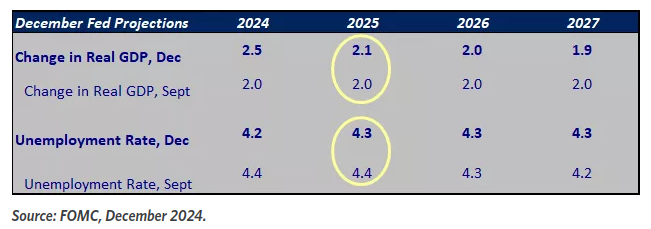

Perhaps the other key takeaway from this week's FOMC meeting is that the Fed believes both the

U.S. economy and the labor market are in good shape, and this was reflected in its updated

projections. Powell noted at the press conference that he is "very optimistic about the economy."

The new Fed forecasts pointed to better economic growth and a lower unemployment rate versus

September estimates. The projections showed U.S. GDP growing by 2.1% in 2025, compared

with 2.0% at the September meeting. In addition, the unemployment rate is now expected to

be 4.3% for 2025, versus 4.4% at the September FOMC meeting. Overall, the resilience of the

U.S. economy should provide the Fed with some comfort that consumers have been able to withstand

the restrictive policy stance thus far.

-

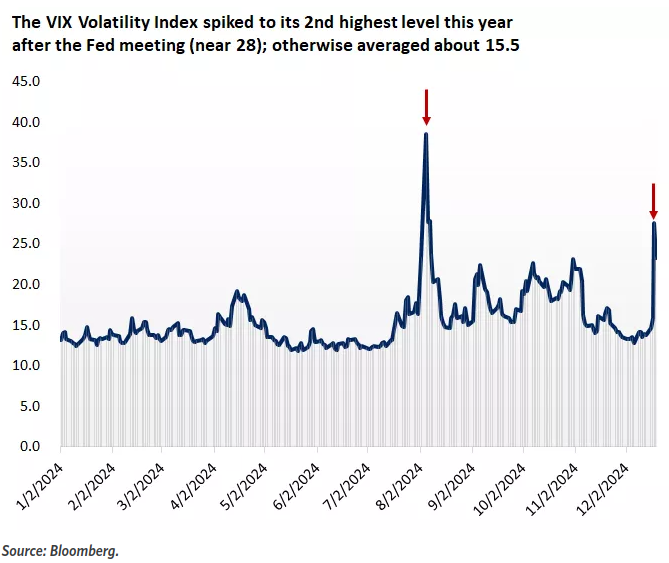

After a 27% gain in the S&P 500 through Monday last week, it is not surprising to see some

pullback in markets, particularly as we head into year-end and investors are thinking about

profit-taking, rebalancing, and tax-loss harvesting.

Keep in mind that even with the pullback we saw after the Fed meeting last week, the S&P 500 is

still up about 24%, and the less tech-heavy Dow Jones Index is up about 14%. From peak to trough,

the decline in the S&P 500 was about 3.5% and about 6% for the Dow Jones, indicating that both

indexes experienced corrections of less than 10%, which are common in most years.

Bond yields have also moved higher, with the 10-year U.S. Treasury yield now above 4.5%. This

move has been driven by a combination of shallower rate-cut expectations, and higher economic

growth and inflation prospects. Nonetheless, for balanced investors, these elevated yields could

present an opportunity to consider gradually moving any outsized positions in cash into the

investment-grade bond market, particularly into seven- to 10-year intermediate bonds.

More broadly, long-term investors in the market should take comfort that despite the volatility

of last week, not much has changed from a fundamental perspective. Markets will most certainly

face new "walls of worry" next year, including uncertainty around government policy and Fed

policy, but we believe the underlying drivers of the bull market remain in place. In

this backdrop, investors can continue to use bouts of volatility and pullbacks as

opportunities, to diversify, rebalance, and add quality investments in both stocks and

bonds – in line with your personal risk tolerances and goals – even if the Fed cuts rates

at a more gradual pace in the year ahead.

-

Manufacturing job openings fell by 13,000 in October, to 465,000, the lowest since September 2020.

Since April 2022, available vacancies in the manufacturing sector have dropped by a whopping 532,000.

In effect, they are now below the 2018 pre-pandemic levels.

In November, manufacturing jobs fell 61,000 year-over-year to 12.9 million, the second-lowest since August 2022.

This marks the 4th consecutive monthly decline in manufacturing employment.

The manufacturing sector is contracting.

-

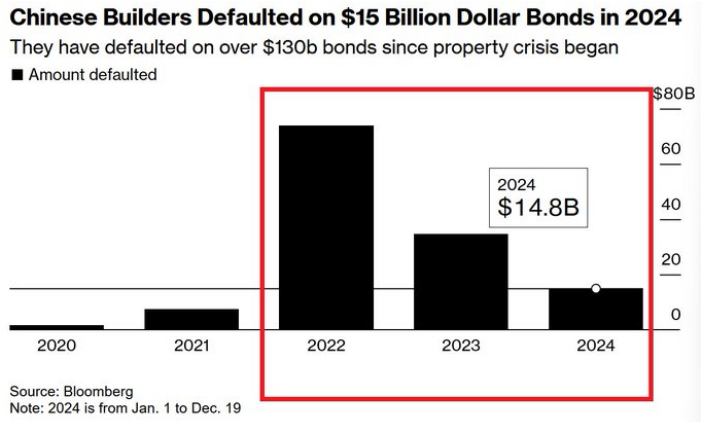

A massive $133 BILLION worth of Chinese builders' bonds have defaulted over the last 5 years.

This year alone $15 billion bonds have gone under.

Property share prices have plummeted by over 90% over the last 5 years.

-

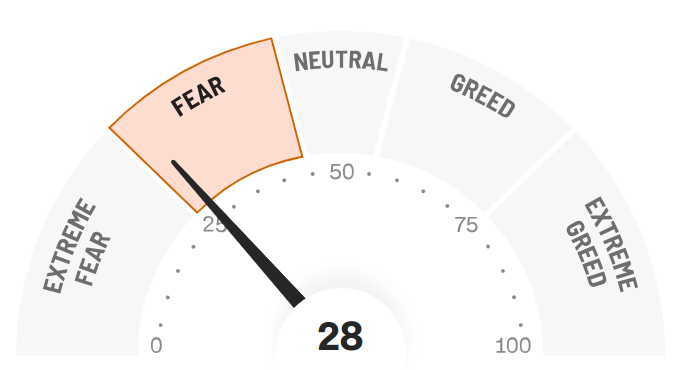

Final Words: Markets are at the all time high and fed is cutting

interest rate, caution warranted. Below is CNN Greed vs Fear Index, pointing at

'fear'. This maybe a good time to buy ETF such as VOO.

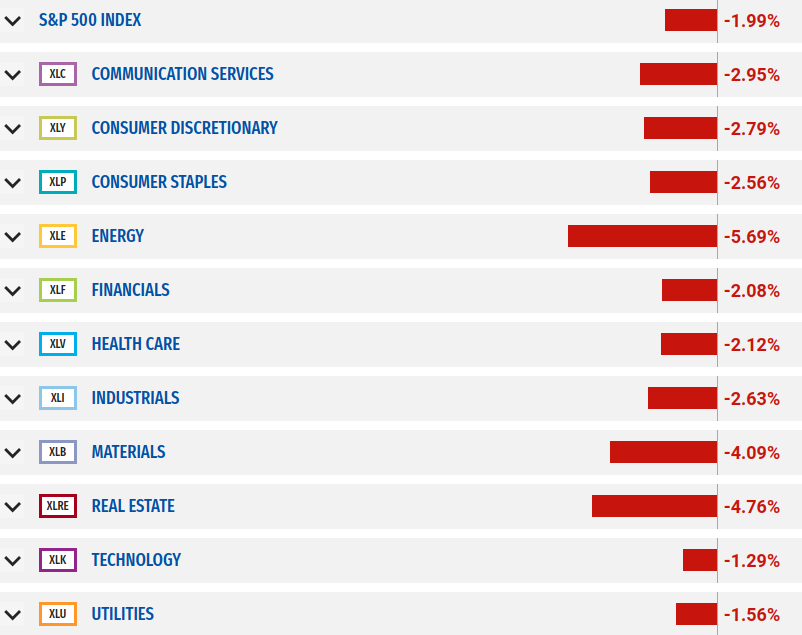

Below is last week sector performance report.

If you are looking for investment opportunities, you can take a look at our

Hidden Gems

section, and if you want to see our past performance, visit our

Past Performance section. If you are looking for

safe and low cost Exchange Traded funds(ETFs), check out our

ETF recommendations.

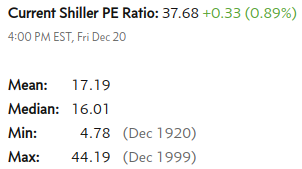

Currrent Shiller PE (see below) is showing overbought conditions as index is far above mean/media

and our AryaFin engine is indicating caution. Have a good weekend.